![]()

Cleft lip and cleft palate are among the most common congenital craniofacial anomalies globally, often requiring surgical intervention within the first year of life and follow-up corrective procedures later. While clinical outcomes and surgical techniques have evolved significantly, procedure volumes remain one of the most reliable indicators of unmet need, healthcare access, and market potential.

This is where procedure-level intelligence becomes critical. By tracking annual surgical volumes across key geographies, stakeholders from medical device companies to healthcare investors can better understand where demand is rising, where systems are saturated, and where growth opportunities exist.

Leveraging insights from BIS Research’s Surgical Procedure Volume Database (SPVD), this article explores how lip repair surgery volumes have evolved globally between 2023 and 2025, and what these trends reveal about the future of cleft care.

Lip repair surgery is a cornerstone procedure in the management of cleft lip and palate, typically performed in infancy but often followed by secondary revisions, palate repair, and speech-related interventions. Procedure volumes are influenced by multiple factors, including:

• Birth prevalence of cleft conditions

• Access to pediatric surgical care

• Public healthcare coverage and NGO involvement

• Advancements in early diagnosis and referral pathways

As healthcare systems mature and awareness improves, procedure volumes tend to increase not necessarily due to higher incidence, but due to better treatment access.

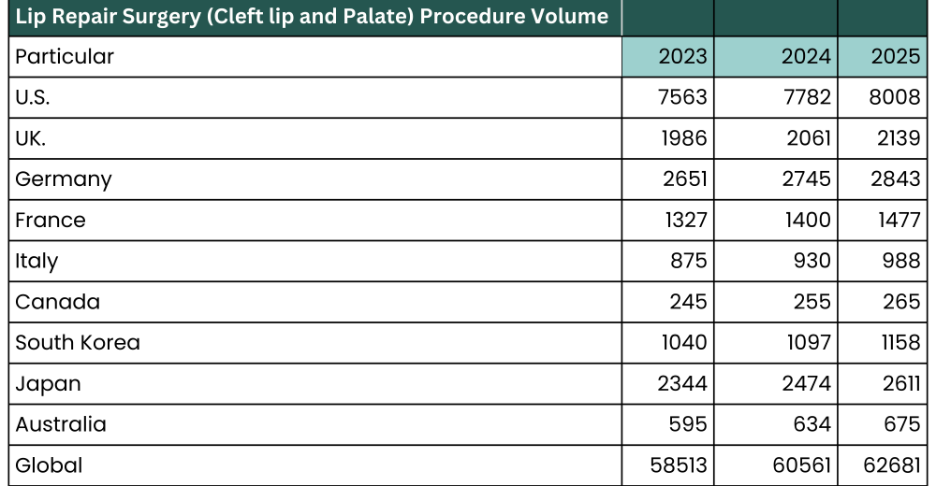

According to BIS Research estimates, global lip repair surgery volumes increased steadily from 58,513 procedures in 2023 to 62,681 procedures in 2025, reflecting a consistent upward trajectory.

This growth highlights two parallel trends:

1. Improved access to surgical care in developed markets

2. Gradual expansion of pediatric surgical capacity in select emerging economies

Rather than sharp spikes, the market shows predictable, incremental growth, making it particularly attractive for long-term strategic planning.

The U.S. remains the single largest market for lip repair surgery, with volumes rising from 7,563 procedures in 2023 to 8,008 in 2025. This growth is supported by:

• Advanced pediatric surgical infrastructure

• Strong insurance coverage for congenital anomalies

• High rates of early diagnosis and intervention

For device manufacturers and service providers, the U.S. represents a stable, innovation-driven market rather than a volume-surge opportunity.

Key European countries including the UK, Germany, France, and Italy demonstrate steady procedural growth over the forecast period.

2023 | 2025 | |

Germany: | 2,651 | 2,843 |

UK | 1,986 | 2,139 |

France | 1,327 | 1,477 |

Italy | 875 | 988 |

These trends refle Tracking Global Demand for Cleft Lip and Palate Surgery Through Procedure Volume Trends (2023–2025) Tracking Global Demand for Cleft Lip and Palate Surgery Through Procedure Volume Trends (2023–2025)

Asia-Pacific markets such as Japan and South Korea show notable volume expansion:

Country | 2023 | 2025 |

Japan | 2,344 | 2,611 |

South Korea | 1,040 | 1,158 |

This growth is driven by:

• Improved neonatal screening

• Rising healthcare expenditure

• Cultural emphasis on early corrective interventions

Although absolute volumes remain lower than Western markets, Asia-Pacific represents a strategic growth frontier, especially for companies targeting long-term expansion.

Countries like Canada and Australia contribute smaller but steadily increasing volumes:

Canada | 245 | 265 |

Australia | 595 | 675 |

These markets are characterized by high treatment standards but limited population size, making them important for validation and pilot adoption rather than large-scale volume play.

Understanding procedure volumes helps align:

• Product launches

• Sales force allocation

• Hospital targeting strategies

Markets with consistent year-on-year growth such as the U.S., Germany, and Japan offer lower risk and predictable demand.

Procedure volume growth acts as a leading indicator of revenue potential, especially in surgical instruments, sutures, and perioperative care solutions. Stable growth in cleft lip repair signals resilience, even during broader healthcare slowdowns.

Accurate volume data supports:

• Capacity planning

• Workforce allocation

• Impact assessment of cleft care programs

It also helps identify regions where surgical access is improving but still underserved.

Traditional market sizing often relies on revenue or incidence alone. However, procedure volume bridges the gap between epidemiology and real-world clinical practice.

The BIS Research Surgical Procedure Volume Database (SPVD) provides:

• Country-level procedure volumes

• Historical and forecast data

• Clinically validated assumptions

This makes SPVD an essential tool for evidence-based decision-making in surgical markets.

Learn more about the database here:

Surgical Procedure Volume Database by BIS Research

Lip repair surgery for cleft lip and palate may not be a high-volatility market but that is precisely its strength. The steady rise in procedure volumes from 2023 to 2025 underscores a dependable, medically necessary segment driven by clinical need rather than discretionary demand.

For stakeholders seeking predictability, resilience, and long-term relevance, lip repair surgery and the data tracking it offers a compelling opportunity.