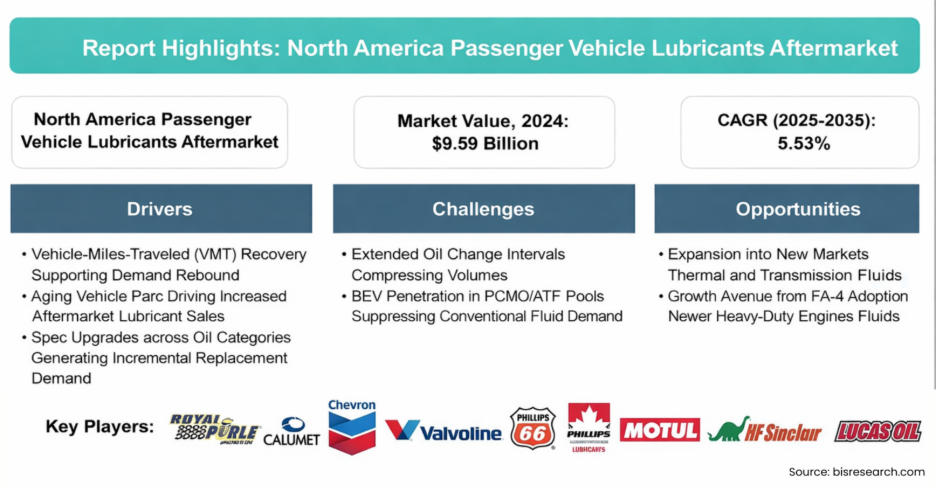

The North America passenger vehicle lubricants aftermarket may not always command the spotlight, but it remains a critical pillar of the region’s automotive ecosystem. In 2024, the market was valued at $9.59 billion, reflecting the essential role lubricants play in maintaining vehicle efficiency, durability, and performance. Looking ahead, the market is set for steady expansion, with revenues projected to reach $17.33 billion by 2035, growing at a compound annual growth rate (CAGR) of 5.53% during the 2025–2035 forecast period.

This growth story of the North America passenger vehicle lubricants aftermarket is rooted in a combination of sustained vehicle usage, rising consumer expectations, and continuous product innovation by leading lubricant manufacturers, who are increasingly focused on enhancing engine protection, fuel efficiency, and compatibility with evolving vehicle technologies.

Passenger vehicles in North America are being driven longer and kept on the road for extended lifespans. As vehicles age, the need for reliable lubrication becomes even more important. Engine oils, transmission fluids, and specialty lubricants reduce friction, manage heat, and protect critical components, directly influencing fuel efficiency and vehicle longevity.

While newer vehicles feature advanced engines and improved efficiencies, they also demand higher-quality and more precisely engineered lubricants. This has elevated the importance of the aftermarket, where vehicle owners rely on trusted brands and service centers to maintain performance well beyond the factory warranty period.

Download the complete Table of Contents for a detailed market overview

The North America passenger vehicle lubricants aftermarket is led by a group of well-established global players, many of whom have built decades-long relationships with consumers and service providers.

1. ExxonMobil Corporation stands out as a market leader through its Mobil™ brand. Known for premium synthetic and semi-synthetic engine oils, ExxonMobil emphasizes fuel efficiency, engine protection, and performance across a wide range of passenger vehicles. Its strong R&D capabilities allow it to continuously adapt formulations to evolving engine technologies.

2. BP PLC, through its Castrol brand, is another dominant force. Castrol’s presence is especially strong in the premium and performance lubricant segment. The brand has positioned itself as a technology-driven partner to both consumers and automakers, offering products designed for modern engines, hybrids, and high-performance vehicles.

3. Shell, via its Shell Helix and related lubricant portfolios, maintains a significant share of the North American aftermarket. Shell focuses heavily on advanced additive technologies that enhance engine cleanliness and reduce wear, appealing to consumers seeking longer drain intervals and consistent performance.

4. Chevron Corporation, with its Havoline brand, is widely recognized across service centers and retail outlets. Chevron benefits from a robust distribution network and a reputation for reliability, making it a preferred choice for everyday passenger vehicle maintenance.

5. Valvoline Inc. holds a unique position in the market by combining lubricant manufacturing with a strong service network. Its direct-to-consumer presence through quick-lube centers strengthens brand loyalty and gives Valvoline valuable insight into evolving consumer maintenance behaviors.

In addition to these giants, Phillips 66, TotalEnergies, Petro-Canada Lubricants, AMSOIL, and other specialty players contribute to market diversity, particularly in high-performance, synthetic, and niche lubricant applications.

Request a sample report to preview key insights and data.

One of the defining characteristics of the lubricants aftermarket today is innovation. Manufacturers are increasingly focused on:

• High-performance synthetic lubricants that offer better thermal stability and engine protection

• Extended oil-drain formulations, appealing to convenience-focused consumers

• Fluids designed for newer powertrain technologies, including hybrids and electric drivetrains

At the same time, regulatory pressure around fuel efficiency and emissions continues to push lubricant producers toward lower-viscosity and environmentally optimized formulations.

With a strong 2024 base of $9.59 billion and a clear path toward $17.33 billion by 2035, the North America passenger vehicle lubricants aftermarket is positioned for resilient, long-term growth. Even as vehicle technologies evolve, the fundamental need for lubrication remains unchanged only the science behind it is becoming more sophisticated.

For industry players, success will depend on brand trust, product innovation, and the ability to adapt to changing vehicle technologies. For consumers, the aftermarket will continue to be where performance, protection, and peace of mind meet one oil change at a time.