The push for a sustainable, low-carbon economy has reached a defining moment in 2025. Industries, governments, and consumers are collectively accelerating innovation across three major themes: the decarbonization of materials, next-generation energy and functional materials, and a sweeping shift toward green and circular chemistry. Each of these themes represents a pivotal area of technological disruption and opportunity, driving new markets and reshaping how we build, power, and sustain our world.

Below, we explore nine transformative technologies and materials each introduced with a clear summary, then deepened by a single, standout trend, market dynamic, or use case. Together, they form the building blocks of a low-carbon future.

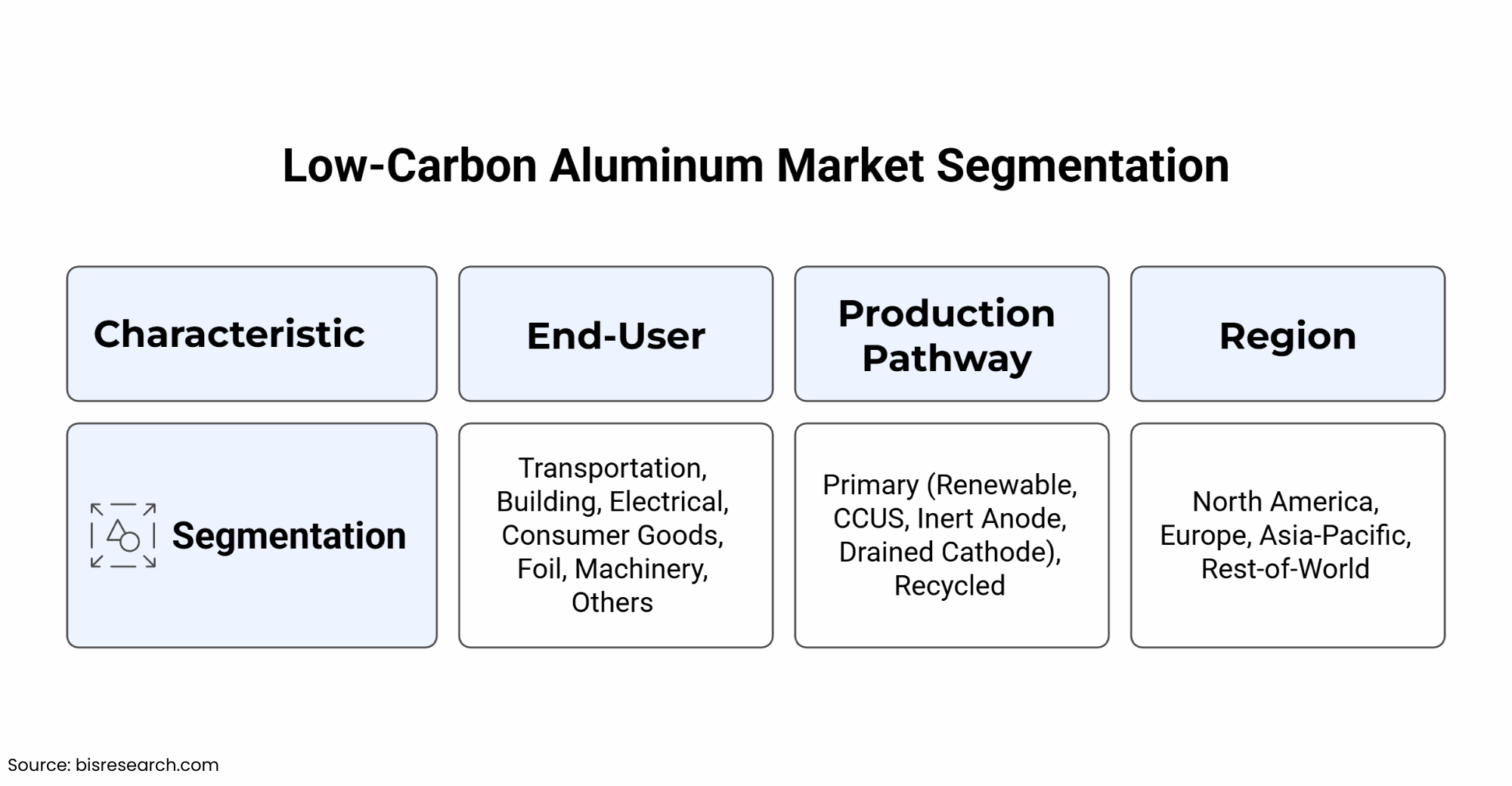

Low-Carbon Aluminum: The Green Metal of Choice

Aluminium is foundational to transportation, construction, electronics, and packaging. Yet, its traditional production is among the most carbon-intensive of any industrial material, mainly due to electricity-hungry smelting processes. The rise of low-carbon aluminium produced with hydropower, solar, or cutting-edge carbon capture signals a seismic shift toward greener supply chains. Global brands are now demanding transparency on carbon content, and the market is responding with innovations that are rewriting the rules of metals production.

Market Dynamic: Supply Chain Pressure and Premium Pricing

According to BIS Research, low-carbon aluminium is not only gaining traction for its environmental credentials but is also rapidly being embedded into global supply chains. The pressure from downstream industries especially automotive and consumer electronics is transforming the competitive landscape. Major automakers and tech giants have set ambitious “zero carbon” goals, which ripple backward to their suppliers. Aluminium producers now face increasing scrutiny regarding their energy sources, with contracts often demanding proof of renewable power and verified low-carbon production. This supply chain accountability, combined with limited green aluminium capacity, is creating a premium market segment. Green aluminium regularly commands higher prices, incentivizing legacy producers to invest in hydropower, solar smelters, and advanced recycling. The result: a virtuous cycle where sustainability drives profitability, not just compliance.

Also read the below:-

1. 5 Game-Changing Companies Leading Asia-Pacific’s Low-Carbon Aluminum Industry

2. Low-Carbon Aluminum Role in Asia-Pacific’s Industrial Transformation

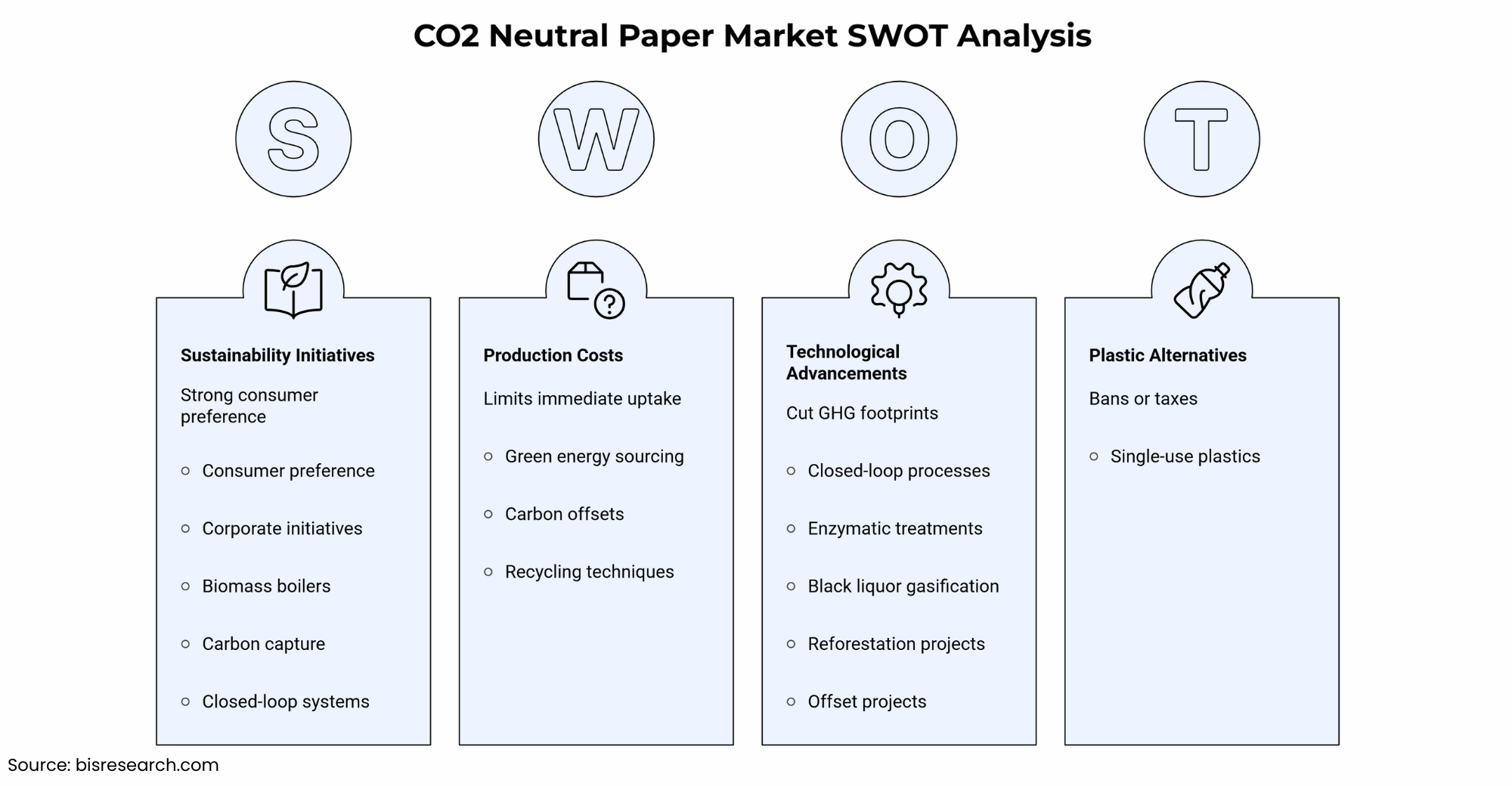

The pulp and paper industry is transforming through a new generation of CO2-neutral products. These papers are made from responsibly sourced fiber, processed using renewable energy, and crucially manufactured with net-zero or even negative carbon emissions. As digital commerce booms, the demand for sustainable packaging grows exponentially, making CO2-neutral paper a vital part of the circular economy and an essential component of brands’ climate pledges.

Use Case: Amazon’s Net-Zero Packaging Revolution

The world’s packaging giants are racing to decarbonize and e-commerce is ground zero. Amazon, for example, is investing heavily in CO?-neutral paper and board for its vast global logistics network. The company’s commitment to “Shipment Zero” (a pledge to make 50% of shipments net-zero by 2030) hinges on a total rethink of paper: from renewable forestry and green energy use, to carbon capture in production and fully recyclable coatings. The real-world impact? Every Amazon package delivered in CO?-neutral paper shifts gigatons of emissions out of the global supply chain. The push has also forced smaller e-retailers and packaging converters to follow suit, turning a green ambition into a market-wide movement. It’s not just about the box; it’s about every link in the chain, from the forest to the customer’s door.

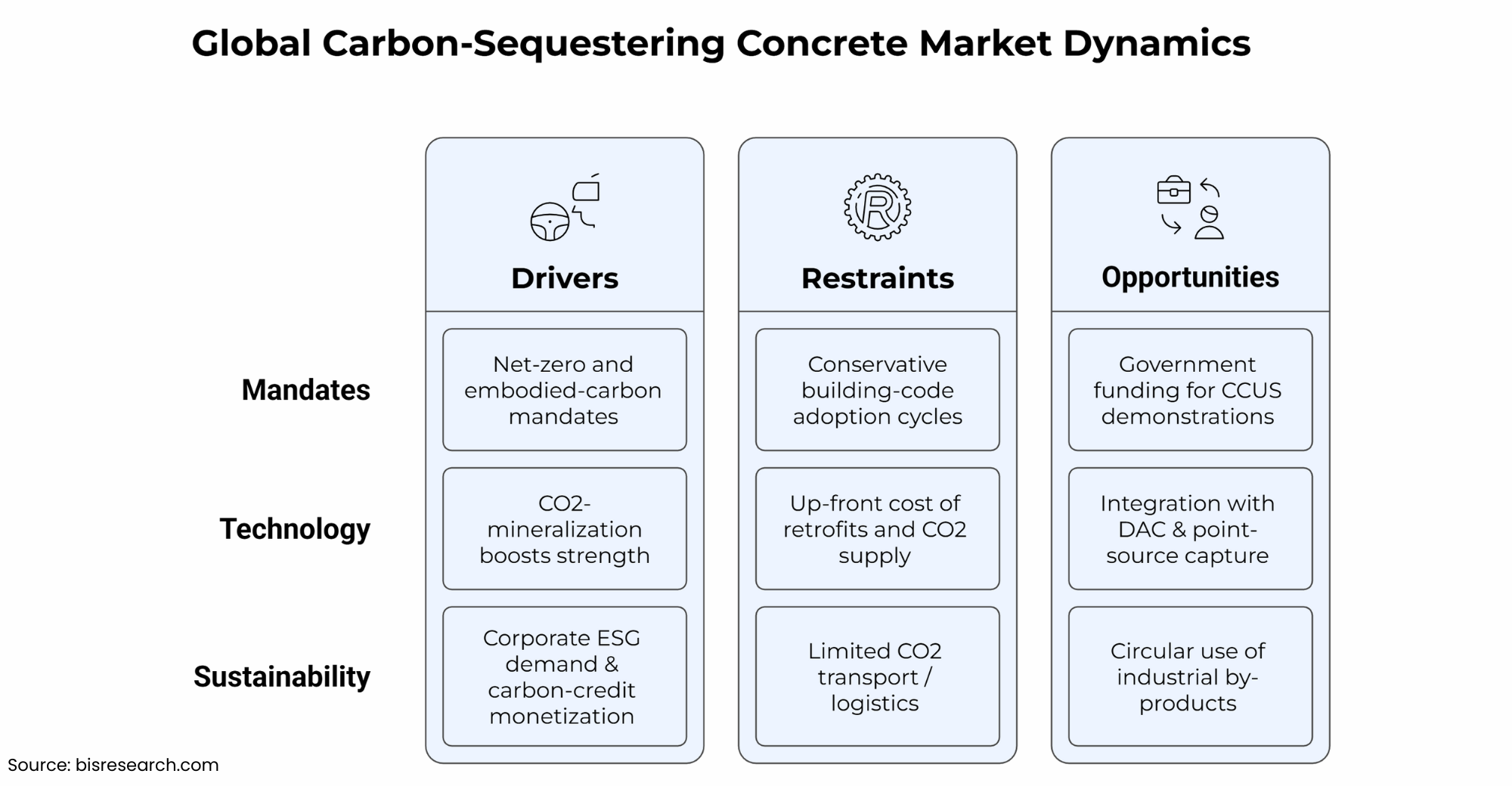

Concrete is the world’s most widely used construction material and one of its largest sources of industrial CO? emissions. Carbon-sequestering concrete uses advanced mineralization and chemical processes to trap CO? within its structure during curing or throughout its service life. This innovation transforms buildings, bridges, and roads into long-term carbon sinks, supporting global net-zero goals while maintaining the strength and durability of conventional concrete.

Also read- Carbon-Sequestering Concrete Market is Estimated to Surge in Next 10 Years

Concrete the backbone of modern civilization is now being reimagined as a carbon storage device. The hottest trend in 2025? “Concrete as a Service” where suppliers guarantee not only the structural performance but also the net carbon sequestration over the lifetime of a building. Here’s how it works: Startups and multinationals are developing mixes that absorb CO? from industrial flue gases or directly from the air, trapping it inside mineral structures as the concrete cures. Innovative service models are emerging: clients pay not just for cubic meters, but for certified tons of CO? locked away. Municipalities and infrastructure funds are incentivizing the use of carbon-sequestering concrete through green bonds and net-negative emissions targets. The business model turns every new bridge or skyscraper into an active weapon against climate change—a concrete step forward, quite literally.

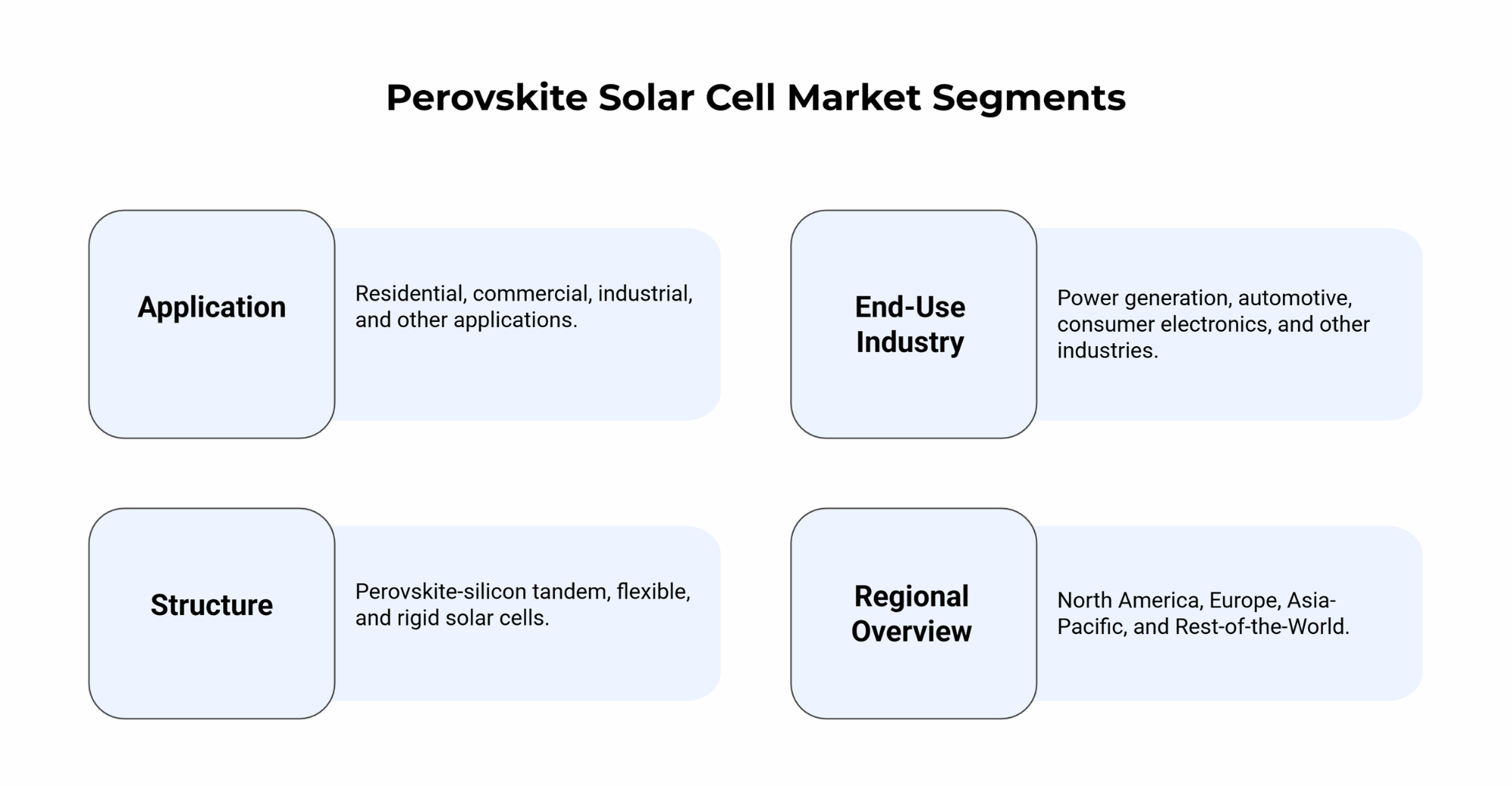

Perovskite Solar Materials: The Next Leap in Photovoltaics

Perovskite solar materials represent a revolution in solar energy generation. Their unique crystalline structure allows for exceptional light absorption and charge transport, offering the promise of higher efficiency and flexibility compared to traditional silicon cells. With the potential for low-temperature, scalable manufacturing, perovskites are poised to transform both utility-scale solar farms and integrated urban photovoltaics.

Trend: Tandem Solar Cells Breaking Efficiency Barriers

If the last decade belonged to silicon, the next belongs to perovskite. The defining trend for perovskite solar cells is their integration into tandem architectures layered on top of traditional silicon cells to capture a broader spectrum of sunlight and break through previous efficiency ceilings. In research labs and pilot lines worldwide, tandem cells have hit efficiency records above 30%, compared to around 22% for the best silicon alone. Companies are now racing to commercialize flexible, lightweight panels for rooftops, vehicles, and even portable devices. Perovskite-silicon tandems can be produced with less energy and fewer emissions, opening doors for urban solar adoption and new business models, such as “solar skins” that blend seamlessly with architecture. This leap isn’t just incremental; it’s redefining what’s possible for solar, with the potential to double global PV output from the same land area or rooftop.

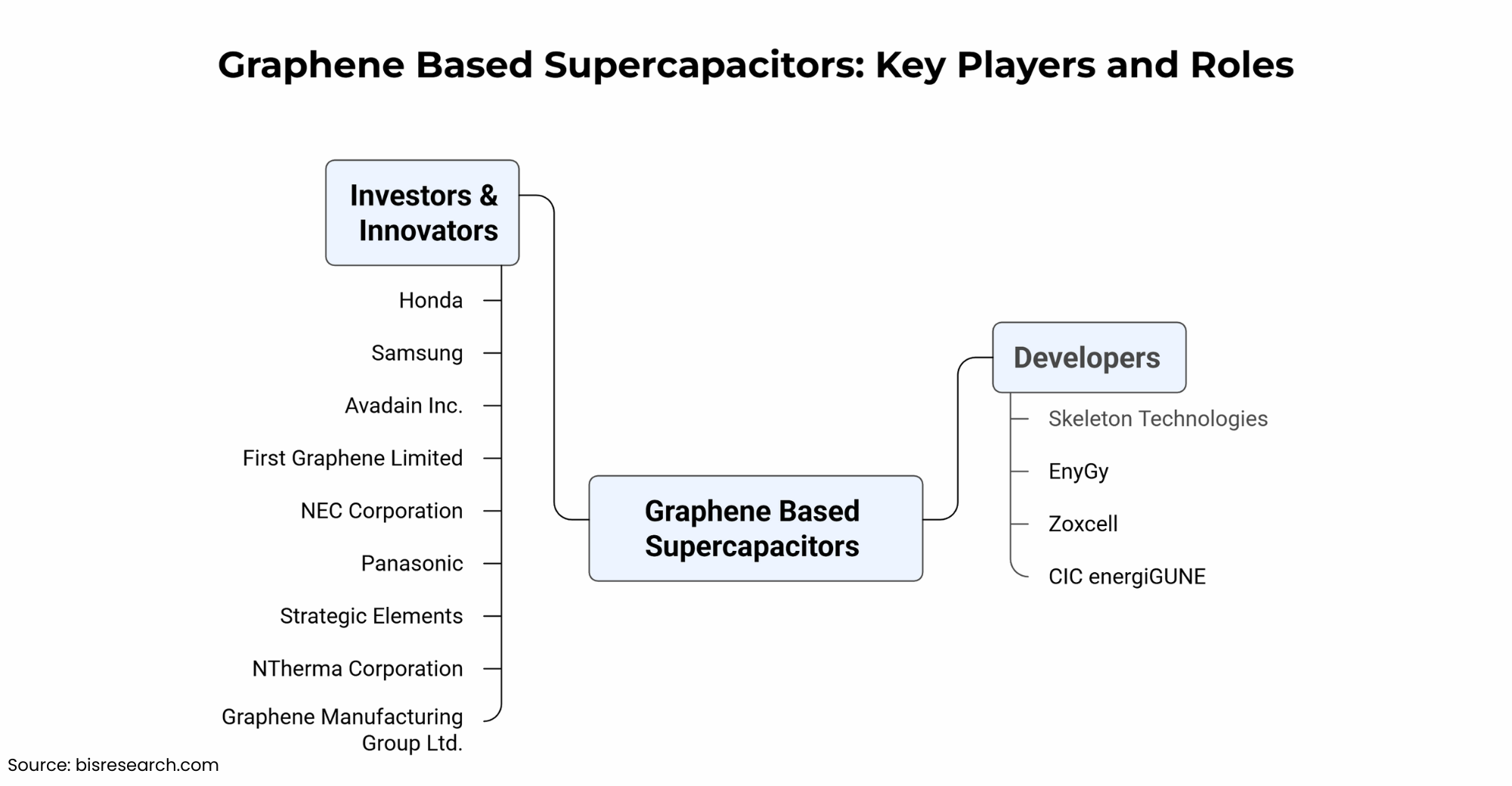

Graphene supercapacitors are a new breed of energy storage device, leveraging the remarkable conductivity and strength of graphene to enable ultra-fast charging, high power output, and long cycle life. Unlike traditional batteries, supercapacitors excel in applications requiring rapid bursts of energy and near-instantaneous recharging, supporting the electrification of transportation and the expansion of smart city infrastructure.

Use Case: Revolutionizing Urban Mass Transit

Supercapacitors made with graphene are disrupting how we store and deliver energy, and nowhere is this more vivid than in urban public transit. Cities like Shanghai and Barcelona have deployed electric buses equipped with graphene supercapacitors, allowing them to recharge in as little as 10–30 seconds at every stop. This ultra-fast charging slashes downtime and eliminates the need for massive onboard batteries. The operational advantages are profound: less weight, higher reliability, and longer life cycles, all with a much lower environmental footprint compared to traditional lithium-ion storage. These buses can run continuous shifts, powered by clean electricity, helping cities decarbonize their transit networks and improve air quality. The story of graphene supercapacitors is the story of electrification without compromise a new era of sustainable mobility.

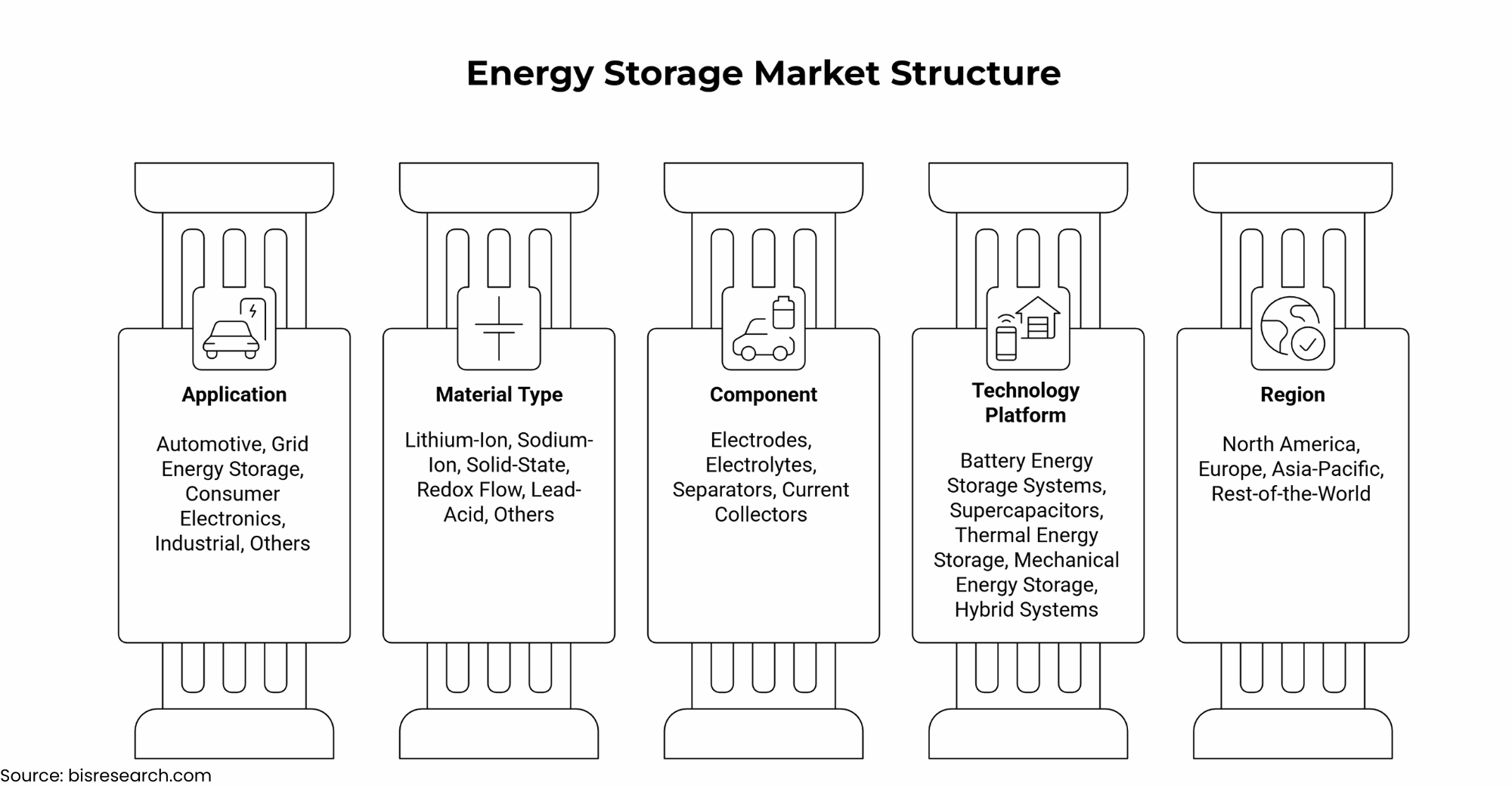

Energy Storage Materials: The Backbone of Renewable Integration

As grids incorporate ever-greater shares of renewable energy, advanced energy storage materials are emerging as the essential buffer between variable supply and steady demand. New chemistries lithium-sulfur, sodium-ion, solid-state promise greater capacity, safety, and sustainability. These materials support not just electric vehicles but also the transformation of national power infrastructure.

Market Dynamic: From Niche to Necessity in Grid Modernization

The rise of renewables like wind and solar has exposed the Achilles’ heel of the traditional grid: variability. In 2025, advanced energy storage materials from sodium-ion to solid-state batteries are transforming from niche technologies to grid-critical infrastructure. Utilities and independent power producers are scrambling to deploy these solutions at every level: residential, commercial, and utility-scale. According to BIS Research, the demand for robust, scalable storage is being fueled by aggressive national targets for renewables, falling battery costs, and mounting pressure to eliminate fossil-fuel peaker plants. Energy storage is no longer an optional upgrade; it’s a core enabler of the clean energy transition, unlocking flexible, resilient, and decarbonized grids. The leaders in storage technology are shaping the future of electricity making blackouts rarer and clean power ubiquitous.

3. Green & Circular Chemistry

Bio-Circular PVC: Plastics Without the Pollution

Polyvinyl chloride (PVC) is one of the world’s most common and controversial plastics. The bio-circular PVC variant addresses two core challenges: sourcing raw materials from renewables (not fossil fuels) and ensuring that every product can be recovered, recycled, and reborn at end-of-life. In the construction, healthcare, and consumer goods sectors, bio-circular PVC is emerging as a key material for circularity and emissions reduction.

Trend: Closing the Loop in Construction Materials

PVC has a notorious reputation for pollution, but bio-circular PVC is changing the narrative especially in construction. The hottest trend? Full-loop circularity, where bio-based PVC is manufactured from renewable feedstocks (like plant oils or waste biomass) and designed for endless recycling at end-of-life. Major building projects in Europe and Asia are already specifying circular PVC for pipes, windows, and flooring. Digital “material passports” track every batch from cradle to grave, ensuring that when a building is renovated or demolished, every scrap of PVC can be recovered and reborn as new product. This closed-loop approach drastically reduces both GHG emissions and landfill waste, aligning with stricter green building codes and customer demands for sustainability documentation. The goal: not just less harmful plastics, but truly waste-free construction.

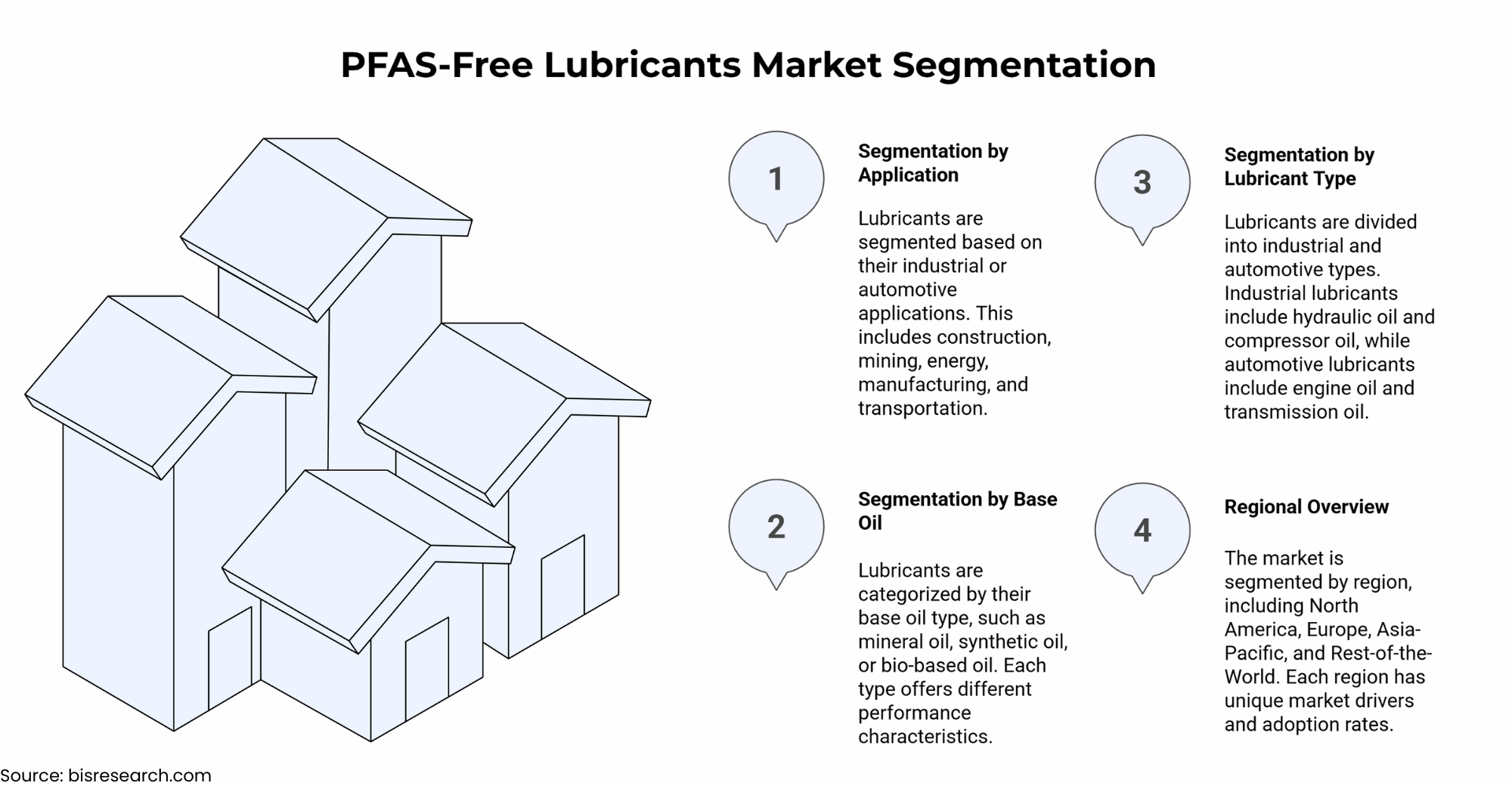

PFAS-free lubricants are the response to growing concerns about persistent, hazardous “forever chemicals.” These next-gen lubricants maintain the performance and longevity of industrial fluids, without leaving a toxic legacy in water, soil, or food chains. They’re vital for industries looking to stay ahead of evolving regulations and safeguard both people and the planet.

Market Dynamic: Regulatory Bans Drive Innovation and Adoption

The chemicals world is in upheaval as regulators clamp down on PFAS persistent, bioaccumulative substances nicknamed “forever chemicals.” The market dynamic for PFAS-free lubricants is shaped by a wave of outright bans and phase-outs across the US, EU, and Asia-Pacific. Companies in aerospace, automotive, and electronics manufacturing are urgently seeking replacements to maintain compliance and market access. This rapid regulatory shift is catalyzing green chemistry innovation: formulators are racing to deliver high-performance, non-toxic alternatives that meet demanding industrial specs without environmental or legal risk. Early adopters gain not only compliance but also a reputational edge, as customers and investors demand clean, safe supply chains. The lubricant sector’s pivot is a cautionary tale and a blueprint for all specialty chemicals in the era of green regulation.

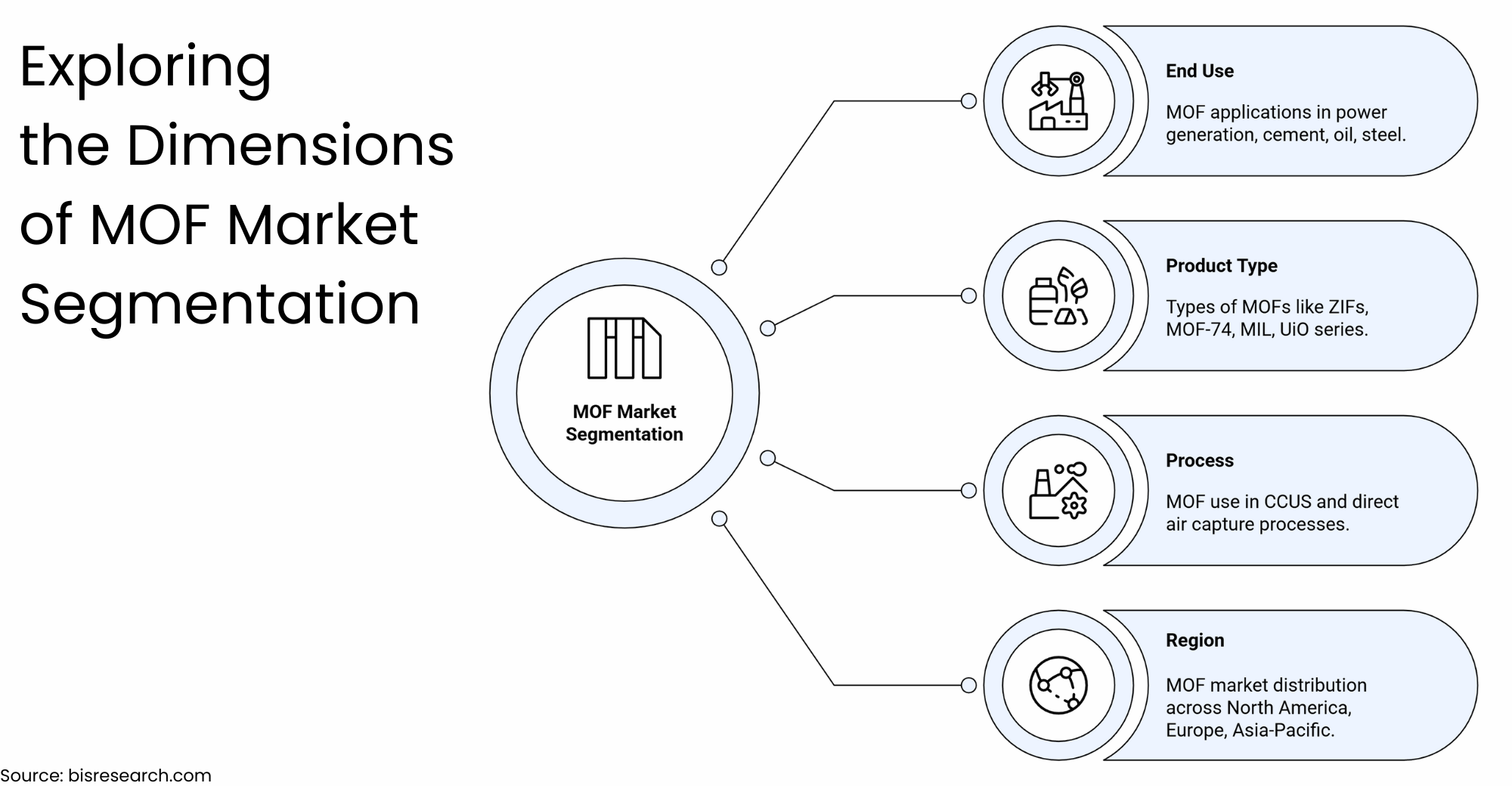

Metal-organic frameworks (MOFs) are ultra-porous crystalline materials with extraordinary surface area, enabling precise and efficient gas separation. MOFs are revolutionizing carbon capture by selectively trapping CO? from industrial flue gases, power plants, and even direct air. Their application is central to carbon-neutral manufacturing and a cornerstone of emerging circular carbon economies.

Use Case: Decarbonizing Cement Plants at the Source

Among the most exciting advances in carbon capture are metal-organic frameworks (MOFs), with their mind-boggling surface area and selectivity for gases. In 2025, MOFs are being piloted to decarbonize one of the hardest sectors: cement production. Global cement plants are testing MOF-based filters to capture CO? directly from kiln exhaust before it enters the atmosphere. The use case is transformative: captured CO? can be compressed and stored underground, or utilized in products such as fuels, chemicals, or even enhanced concrete closing the loop on industrial carbon. By tackling emissions at their source, MOFs enable deep decarbonization in sectors previously considered “too hard to abate.” The success of these pilots could tip the balance in the world’s fight against industrial climate change.

The journey to a low-carbon, circular future is being written in the labs, factories, and boardrooms of today. What do the next few years hold?

Markets will reward pioneers—Those who invest early in green technologies, secure sustainable supply chains, and embrace circular models will win contracts, customers, and market share.

Regulation is accelerating—What is voluntary today (eco-labels, green bonds, Scope 3 accounting) will become mandatory tomorrow. The smart money is on compliance by design, not by afterthought.

Collaboration is key—No single company can close the loop or decarbonize alone. Strategic alliances, cross-sector consortia, and public-private partnerships will define success.

Technology is the enabler—From AI-driven recycling to molecular breakthroughs in chemistry, continuous innovation will separate leaders from laggards.

The shift to advanced materials, sustainable chemistry, and circular manufacturing is the industrial revolution of our age. What makes 2025 different is not just the urgency of climate action, but the rich ecosystem of solutions each with a unique story, challenge, and opportunity emerging across Advanced Materials, Chemicals & Fuels. Whether you’re a manufacturer, policymaker, investor, or innovator, the message is clear: the time for incrementalism is over. The age of low-carbon, circular, and high-performance materials has arrived. Those who embrace it will shape the economy and the environment for decades to come.