A quick peek into the report

Waste-to-Hydrogen Market Overview

Introduction of Waste-to-Hydrogen Market

The waste-to-hydrogen market comprises innovative technologies that convert municipal solid waste, biomass, and industrial residues into clean hydrogen fuel, supporting the global transition toward low-carbon energy. This market has been driven by the increasing need for sustainable waste management and the rising demand for alternative energy sources to reduce greenhouse gas emissions. Advanced processes such as gasification, plasma conversion, and thermochemical treatment play a vital role in enabling efficient and cost-effective hydrogen production. The market is highly competitive, with companies introducing modular systems, scalable plants, and integrated waste-to-hydrogen solutions tailored for industrial and urban applications. Growing emphasis on energy security, circular economy practices, and government-backed hydrogen initiatives further accelerates adoption. Innovations in carbon capture, artificial intelligence-based process optimization, and decentralized plant designs are addressing both environmental concerns and operational challenges. As a result, the market continues to evolve rapidly, shaping the future of clean energy supply while supporting the dual goals of sustainable waste reduction and hydrogen-based decarbonization.

Market Introduction

The waste-to-hydrogen market plays a crucial role in transforming waste management practices into clean energy solutions that support global decarbonization goals. With the growing demand for sustainable fuels and the urgent need to reduce landfill use, the market has been experiencing steady growth. Advanced technologies such as gasification, plasma conversion, and thermochemical treatment are increasingly adopted for efficient and reliable hydrogen production from waste streams. These innovations help optimize energy recovery, lower carbon emissions, and improve the economics of waste-to-hydrogen projects, driving market expansion.

The market also benefits from rising government investments in clean hydrogen strategies and the transition toward circular economy models. As a result, utilities, technology developers, and energy companies are prioritizing the integration of solutions to strengthen energy security and reduce environmental impact. With continuous innovation and supportive policies, the waste-to-hydrogen market is expected to grow rapidly as a cornerstone of the clean energy transition.

Industrial Impact

The waste-to-hydrogen market has been witnessing steady growth driven by the rising demand for sustainable energy, green hydrogen, and efficient waste management solutions. Technologies are essential for addressing both environmental concerns and energy needs by converting municipal solid waste, biomass, and industrial residues into clean hydrogen fuel. The market is evolving rapidly with the integration of advanced processes such as gasification, plasma conversion, and thermochemical treatment. These innovations enable more efficient, scalable, and cost-effective hydrogen production compared to conventional methods of waste disposal and energy generation. Furthermore, increasing investments in renewable energy projects and circular economy initiatives have been fuelling the adoption of waste-to-hydrogen solutions worldwide. Industries are prioritizing low-carbon strategies, including the use of hydrogen fuel cells, to reduce emissions, enhance energy security, and meet global decarbonization targets. As governments and corporations focus on sustainable growth, the market is expected to play a significant role in reshaping the energy and waste management sectors in the coming years.

Market Segmentation:

Segmentation 1: By Application

• Chemical Production

• Power and Energy Storage

• Transportation/Mobility

• Refining Industry

• Others

Chemical Production to Dominate the Waste-to-Hydrogen Market (by Application)

The market, by application, has been predominantly driven by chemical production. The chemical production segment was valued at $12.8 million in 2024 and is projected to reach $275.4 million by 2035, exhibiting a robust CAGR of 32.72%. This segment’s strong growth is attributed to the critical role that hydrogen plays in various chemical manufacturing processes, making its production essential for ensuring the sustainability and efficiency of the chemical industry. Moreover, the increasing demand for clean hydrogen as an industrial feedstock, coupled with investments in advanced waste-to-hydrogen technologies and government incentives for green hydrogen production, further accelerates market expansion. These factors combined underline why chemical production is expected to dominate the market over the forecast period.

Segmentation 2: By Technology

• Anaerobic Digestion

• Gasification

• Pyrolysis

• Others

Segmentation 3: By Waste Type

• Biomass

• Industrial Waste

• Municipal Solid Waste (MSW)

• Wastewater Treatment Residues

• Others

Segmentation 4: By Region

• North America

• Europe

• Asia-Pacific

• Rest-of-the-World

Recent Developments in the Waste-to-Hydrogen Market

• On June 11, 2024, the U.S. Department of Energy (DOE) allocated $9.3 million to six projects aimed at advancing the waste-to-hydrogen market. These projects will focus on converting diverse waste feedstocks into clean hydrogen, supporting decarbonization goals while reducing landfill dependency. By integrating carbon capture with hydrogen production, the initiatives are expected to enhance performance, create local economic opportunities, and strengthen the growth of the waste-to-hydrogen market.

• On October 7, 2025, Air Liquide announced a nearly $50 million investment to strengthen its U.S. Gulf Coast hydrogen network, securing new long-term supply agreements with major refiners. By upgrading pipelines, compression, and distribution systems, the company is expanding capacity with minimal new development. This move highlights growing opportunities in the waste-to-hydrogen market, as enhanced infrastructure ensures a reliable, flexible, and sustainable hydrogen supply for industrial partners.

• On December 10, 2024, German researchers introduced a new biotechnological process to convert wood waste into biohydrogen, supporting the growth of the waste-to-hydrogen market. Developed by the Fraunhofer Institute for Interfacial Engineering, the Institute for Manufacturing Engineering and Automation, and the University of Stuttgart, the method uses bacteria to extract hydrogen from wood-derived sugars. Backed by a $12.7 million investment from the German Federal Ministry of Education and Research, the project is expected to boost green hydrogen production in the Black Forest region.

• On June 25, 2025, Germany’s new government announced significant budget cuts impacting the hydrogen sector, including the waste-to-hydrogen market. The revised plan allocates $1.46 billion for 2026–2032, down from the previous $4.3 billion, while maintaining $571.8 million in 2025 for IPCEI projects linked to renewable hydrogen and infrastructure. Although the national hydrogen strategy aims for 10GW of electrolyzer capacity by 2030, delays in launching key programs raise concerns, with projections suggesting Germany may achieve less than half the target.

Analyst’s Thoughts

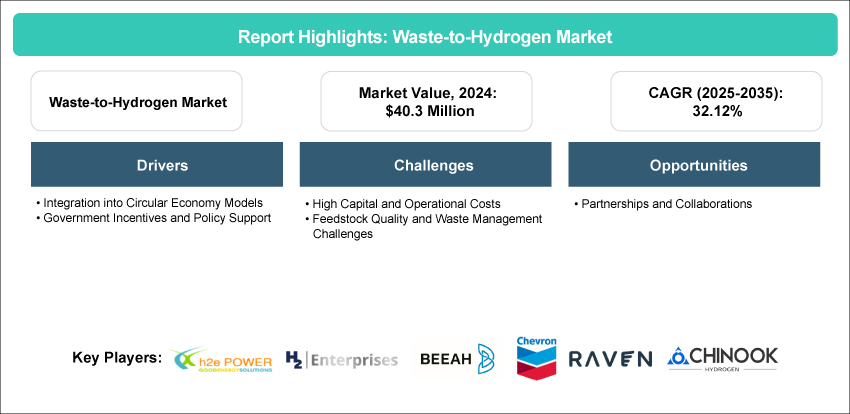

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, “The waste-to-hydrogen market has been growing steadily as demand for sustainable energy and efficient waste conversion technologies increases. The market is projected to expand at a compound annual growth rate (CAGR) of 32.12%. Growth has been driven by advancements in gasification, plasma conversion, and thermochemical processes, enabling scalable and cost-effective hydrogen production. Companies are focusing on innovative technologies and integrated solutions to meet the rising need for clean energy in the market.”

Waste-to-Hydrogen Market - A Global and Regional Analysis

Focus on Application, Technology, Waste Type, and Country-Level Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

Waste-to-hydrogen products are clean hydrogen fuels generated by converting waste materials such as municipal solid waste, agricultural residues, and biomass into hydrogen using advanced thermochemical or biological processes. These products support decarbonization by reducing landfill use while supplying sustainable hydrogen for power, mobility, and industrial applications. The market offers several types of solutions. Gasification-based systems convert organic waste into syngas, which is further processed to extract hydrogen. Plasma gasification technologies use high-temperature plasma arcs for efficient hydrogen recovery. Thermochemical conversion systems optimize hydrogen yield by breaking down complex waste streams. Biological processes leverage microbes and enzymes to produce hydrogen from organic feedstocks. Additionally, modular and decentralized waste-to-hydrogen solutions are emerging, enabling localized energy generation with reduced costs. Together, these technologies are driving innovation and competitiveness in the market.

In the waste-to-hydrogen market, existing players are adopting multiple strategies to strengthen their competitive position. Many companies are investing in advanced gasification and plasma technologies to improve efficiency and reduce production costs. Strategic collaborations and public-private partnerships are being formed to secure funding and scale pilot projects into commercial plants. Firms are also focusing on modular and decentralized solutions to provide flexible and region-specific applications. Another key strategy is the integration of carbon capture and storage (CCS) with waste-to-hydrogen projects to meet stringent emission targets and enhance environmental performance. Market leaders are expanding their portfolios by combining hardware, software, and AI-based process optimization for better yield management. In addition, global players are pursuing geographic expansion through joint ventures and long-term supply agreements to secure demand in industrial, mobility, and energy sectors. Collectively, these strategies are shaping the competitive growth of the market.

A new company entering the market can stay competitive by focusing on innovation and niche opportunities. Developing low-cost, high-efficiency gasification or plasma conversion technologies can help differentiate its offerings. Targeting modular and decentralized waste-to-hydrogen solutions would enable localized energy generation, appealing to municipalities and small industries seeking cost-effective options. The company could also emphasize integration of carbon capture and storage (CCS) to meet tightening emission regulations and attract sustainability-focused investors. Leveraging AI-driven process optimization for improved hydrogen yield and operational efficiency presents another strong opportunity. Building strategic partnerships with utilities, governments, and industrial players can secure funding and long-term demand. In addition, entering emerging markets with high waste generation but limited clean energy infrastructure could provide early-mover advantages. By aligning with global decarbonization and circular economy goals, the new entrant can establish a strong foothold in the market.

The market is currently at an emerging stage, but is expanding at a rapid pace due to the rising global focus on clean energy and sustainable waste management. The market has been witnessing strong interest from both established energy corporations and innovative startups, driving competition and technological advancement. With increasing government support, pilot projects are transitioning into large-scale commercial facilities, strengthening the market outlook. The growth of the market is further supported by advancements in gasification, plasma conversion, and thermochemical processes, which are making hydrogen production more efficient and cost-effective. Rising adoption across industries such as power generation, transportation, and heavy manufacturing is creating new opportunities for market players. Strategic partnerships, joint ventures, and public-private collaborations are also accelerating deployment. Overall, the market is expected to experience strong and sustained growth, positioning it as a critical pillar of the global hydrogen economy.

The waste-to-hydrogen market features a mix of established energy corporations, technology innovators, and specialized waste management companies. Key players include SGH2 Energy Global Corp., Powerhouse Energy Group, Raven SR, Boson Energy, and Ways2H, all of which are advancing proprietary technologies for hydrogen generation from waste. Companies such as Air Liquide, Chevron, and SUEZ are strengthening their presence by leveraging existing infrastructure and entering strategic long-term agreements.

The waste-to-hydrogen market has been evolving rapidly, shaped by major trends and strong growth drivers. One of the most significant trends is the adoption of advanced gasification and plasma technologies, which enhance hydrogen yield while minimizing emissions. Another key trend is the rise of modular and decentralized solutions, enabling localized energy production and reducing transportation costs. The integration of artificial intelligence and digital monitoring systems is also improving process efficiency and operational scalability. A critical driver of the market is its alignment with circular economy models, where waste is transformed into valuable clean energy, reducing landfill dependency and environmental impact. Equally important are government incentives and policy support, including subsidies, funding programs, and hydrogen roadmaps that accelerate adoption. Together, these trends and drivers are fostering innovation, attracting investment, and positioning the market as a vital component of the global energy transition.

The market is expanding rapidly, but several challenges continue to hinder its large-scale deployment. One of the primary restraints is the high capital and operational costs associated with building advanced gasification, plasma, and thermochemical facilities. These expenses make commercialization difficult, particularly for new entrants and smaller players without strong financial backing. Another key challenge in the waste-to-hydrogen market is the issue of feedstock quality and waste management, as inconsistent composition of municipal or industrial waste directly impacts hydrogen yield and process efficiency. Securing a reliable and sustainable supply of waste feedstocks requires robust collection, sorting, and preprocessing infrastructure, which adds to the complexity. Additionally, regulatory uncertainties and delays in permitting can slow project development. Together, these challenges create barriers to scalability, even as innovation and policy support continue to drive the market forward.

The market presents significant opportunities for growth as global demand for clean energy and sustainable waste management intensifies. One of the most promising opportunities lies in partnerships and collaborations among technology providers, energy corporations, waste management firms, and government agencies. Such alliances enable companies to pool resources, share expertise, and accelerate the commercialization of waste-to-hydrogen projects. Collaborative ventures also provide access to funding, policy support, and large-scale infrastructure that individual firms may struggle to achieve independently. In the market, partnerships help overcome feedstock challenges by integrating waste collection systems with hydrogen production facilities. Moreover, international collaborations open doors to new markets and facilitate the transfer of advanced technologies across regions. As governments and industries intensify their focus on decarbonization, strategic partnerships will remain a key driver of innovation, scale, and long-term success in the market.

Some of the USPs of the waste-to-hydrogen market report are:

• A dedicated section on growth opportunities and drivers

• A qualitative and quantitative analysis of the waste-to-hydrogen market based on products and applications

• Trend and challenge analysis of different countries, which includes:

o U.S.

o Canada

o Mexico

o Germany

o France

o U.K.

o Italy

o Rest-of-Europe

o China

o India

o Japan

o South Korea

o Rest-of-Asia-Pacific

o Middle East and Africa

o South America

• Regional and country-level forecast

• Pricing Forecasting

• A detailed company profile comprising established players and some startups that are capable of significant growth, along with an analyst's view

Companies developing waste-to-hydrogen products, hydrogen technology providers, government and regulatory bodies, R&D institutions, and feedstock providers should buy this report.