A quick peek into the report

North America Electric Vehicle Battery Components Market Overview

Introduction of the North America Electric Vehicle Battery Components Market

The North America electric vehicle battery components market underpins the region’s transition to electrified mobility by supplying the housings, busbars, stamped structures, thermal systems, cell materials, and management electronics that convert cell chemistry into safe, road-ready propulsion. Demand spans the full spectrum of EV platforms, including two- and three-wheelers, passenger cars, commercial trucks and buses, and off-road equipment, and cuts across multiple chemistry families, covering lithium-ion dominant, with legacy lead-acid and emerging chemistries, cell formats (cylindrical, pouch, prismatic), and materials (aluminum housings to copper/aluminum busbars and anode/cathode inputs). The market’s evolution is shaped by localization of supply chains, rapid advances in performance and safety, and pack-level architecture shifts toward cell-to-pack and structural integration, all while policy, tariffs, and content rules push production closer to vehicle assembly across the U.S., Canada, and Mexico.

Market Introduction

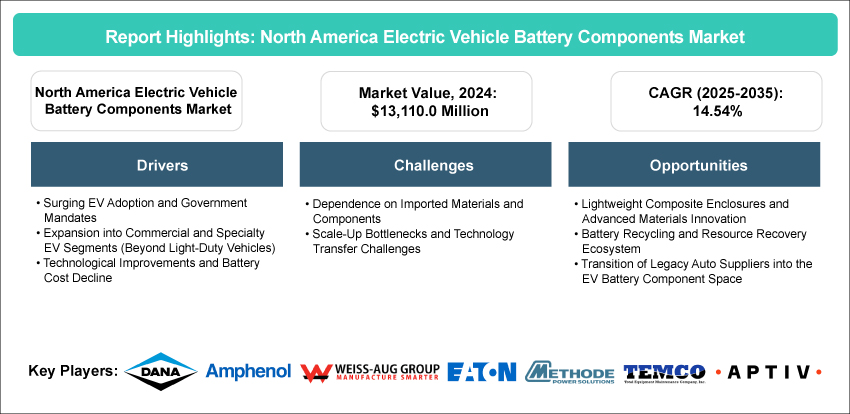

In 2024, the North America electric vehicle battery components market totaled $13.11 billion. Under the realistic scenario, the market is projected to reach $59.85 billion by 2035, supported by a 14.54% CAGR (2025–2035). Growth reflects surging EV adoption, large-scale investment in localized cell and component manufacturing, and technology improvements that increase energy density, reduce cost, and raise safety margins. Segment expansion beyond light-duty vehicles into commercial fleets and specialty/off-road applications further broadens the addressable base, with larger pack sizes amplifying component intensity per vehicle. Structurally, value increase over a period of time across the stack; core electro-materials (anode/cathode) remain the largest slice, while housings, busbars, stamped structures, thermal systems, and BMS hardware scale alongside new gigafactories and pack lines across the region.

The North America electric vehicle battery components market near-term impact is most visible in program cadence, pack performance, and procurement economics. Higher energy density and structural integration (cell-to-pack/cell-to-chassis) free mass and volume that can be redeployed to range or payload, while modular busbar and thermal designs simplify assembly and service. AI-enabled BMS and tighter thermal envelopes improve availability and safety at higher charge rates, supporting faster commissioning and fleet uptime. For procurement, IRA/USMCA content rules and 2024–2025 tariff actions on cells, materials, and sub-assemblies are reshaping award criteria; alongside price, OEMs emphasize domestic footprint, certification against evolving safety standards, traceability, and recycled content pathways to preserve consumer credit eligibility. These forces shorten supplier lists, favor scale players and qualified new entrants, and move award timing earlier in vehicle development as pack architectures converge around standardized interfaces (e.g., NACS-aligned charge ports) and validated enclosure/venting strategies.

Industrial Impact

The industrial footprint is expanding at unprecedented speed. Since 2021, North America has announced scores of gigafactories, cathode/anode plants, separator lines, foil facilities, enclosure casting and machining sites, and recycling hubs, often co-located with OEM assembly campuses. Legacy suppliers are pivoting aggressively; die-casters, stampers, and wiring specialists are retooling into battery housings, structural trays, laminated busbars, and high-voltage interconnects, while materials firms scale cathode precursors and silicon-enhanced anodes. This investment realigns value capture from imports toward regional ecosystems, builds resiliency against global shocks, and seeds long-term capability in midstream processes where historic gaps were most acute.

Market Segmentation:

Segmentation 1: by Vehicle Type

• Electric Two-Wheeler

• Electric Three-Wheeler

• Electric Passenger Vehicles

• Electric Commercial Vehicles

• Electric Off-Road Vehicles

Electric Passenger Vehicles to Dominate the North America Electric Vehicle Battery Components Market (by Vehicle Type)

In the North America electric vehicle battery components market, electric passenger vehicles are projected to remain the dominant segment, growing from $12,779.7 million in 2024 to $55,862.2 million by 2035. This dominance reflects the large installed base and ongoing expansion of passenger EV programs, where pack sizes, housings, and anode/cathode content account for the bulk of component demand. Meanwhile, electric commercial vehicles are anticipated to post the fastest growth, expanding from $199.2 million in 2024 to $2,758.7 million by 2035, driven by the electrification of delivery fleets, heavy trucks, and buses. Electric off-road vehicles also show outsized growth potential, rising from $39.3 million in 2024 to $678.5 million by 2035 as mining, construction, and agricultural sectors pursue electrification. Two- and three-wheelers expected to grow from smaller bases ($65.5 million and $26.2 million in 2024) but will likely expand to $353.7 million and $200.9 million, respectively, by 2035. Together, these trends show that while passenger vehicles anchor market value, growth momentum is shifting toward commercial and specialty applications with higher component intensity.

Segmentation 2: by Battery Chemistry

• Lead Acid

• Lithium-Ion

• Others

Lithium-Ion to Lead the North America Electric Vehicle Battery Components Market (by Battery Chemistry)

The lithium-ion segment is projected to dominate the North America electric vehicle battery components market, expanding from $12,258.0 million in 2024 to $58,190.4 million by 2035. Its leadership reflects broad adoption across passenger and commercial EVs, supported by both high-nickel chemistries for range and lithium-iron-phosphate (LFP) for cost and durability. In contrast, lead-acid batteries are projected to grow modestly from $550.5 million in 2024 to $1,112.2 million by 2035, largely limited to auxiliary and low-voltage applications. The others category (including emerging chemistries and legacy NiMH) is expected to rise from $301.5 million in 2024 to $551.4 million by 2035, remaining niche but strategically important for innovation.

Segmentation 3: by Cell Format

• Pouch Cell

• Cylindrical Cell

• Prismatic Cell

• Others

Cylindrical Cell to Dominate the North America Electric Vehicle Battery Components Market (by Cell Format)

Cylindrical cells hold the largest market share in the North America electric vehicle battery components market, growing from $6,396.4 million in 2024 to $26,526.2 million by 2035, supported by deep manufacturing maturity and scaling of 4680-class production. Prismatic cells, however, are projected to experience the fastest growth, rising from $2,034.3 million in 2024 to $21,503.1 million by 2035, as automakers increasingly adopt cell-to-pack and structural pack designs. Pouch cells are expected to expand steadily from $4,089.5 million in 2024 to $10,317.5 million by 2035, maintaining relevance in space-efficient architectures. The others category expected to grow from $589.8 million to $1,507.1 million, underscoring the diversity of form factors in the evolving EV ecosystem.

Segmentation 4: by Component

• Battery Housing

• Busbars

• Stamping Components (Excluding Busbar Stamping)

• Others (Anode and Cathode)

Anode and Cathode Materials to Dominate the North America Electric Vehicle Battery Components Market (by Component)

Among all components, anode and cathode materials represent by far the largest and most critical value pool in the North America electric vehicle battery components market. In 2024, this segment accounted for $11,405.7 million, and it is projected to reach $53,463.7 million by 2035, making it the backbone of the regional supply chain. These electrode materials are fundamental to both cost structure and performance, and they are closely tied to compliance with IRA requirements, making them essential for OEMs aiming to qualify vehicles for consumer incentives. The sharp growth reflects the scale of EV deployment in the region and the strategic push to localize midstream processing of lithium, nickel, cobalt, and graphite.

Segmentation 5: by Material Type

• Battery Housing Materials

o Steel

o Aluminum

o GFRP

o CFRP

• Busbar Materials

o Cooper

o Aluminum

o Others

• Others (Anode and Cathode Materials and Stamping Components)

o Cobalt

o Lithium

o Natural Graphite

o Manganese

o Others

The battery housing materials segment is expected to grow from $655.5 million in 2024 to $2,719.6 million by 2035 in the North America electric vehicle battery components market, led by aluminum, which expanded from $524.3 million to $2,155.7 million, supported by lightweighting, corrosion resistance, and recyclability. Steel contributed $98.3 million in 2024 and is expected to grow $358.6 million by 2035, retaining importance in rugged, cost-sensitive applications. Composites such as GFRP and CFRP, scaled from $19.8 million and $13.1 million in 2024, are expected to grow $112.5 million and $92.7 million by 2035, respectively, offering thermal and weight advantages in advanced housings.

Segmentation 6: by Country

• U.S.

• Canada

• Mexico

U.S. to Dominate the North America Electric Vehicle Battery Components Market (by Country)

The U.S. is projected to remain the largest and most influential market within North America electric vehicle battery components market. In 2024, the U.S. accounted for $13,107.4 million, and by 2035, this figure is forecasted to rise to $53,270.0 million, underscoring its central role in the region’s electrification strategy. This growth is anchored by large-scale gigafactory investments from both domestic players and international joint ventures, coupled with strong policy support under the Inflation Reduction Act (IRA). Incentives tied to local sourcing, content rules, and recycling integration have incentivized OEMs and Tier 1 suppliers to localize critical parts of their supply chains in the U.S.

Demand: Drivers, Limitations, and Opportunities

Market Demand Drivers: Rapid Electrification, Policy Support, and Localization

The North America electric vehicle battery components market is experiencing strong demand growth, driven by a convergence of technological, regulatory, and strategic factors. One of the primary drivers is the rapid electrification of passenger vehicles, which continues to anchor the market with large-scale volumes and well-established programs. This demand is being reinforced by the accelerated adoption of commercial fleets, particularly delivery vans, buses, and heavy trucks, where larger battery packs amplify demand for housings, busbars, and high-value electrode materials.

Government policy is another key demand driver. The U.S. Inflation Reduction Act (IRA) has created powerful incentives for both consumers and manufacturers, with credits tied directly to domestic content, critical minerals, and recycling. These measures, combined with USMCA rules of origin and additional tariffs on imported cells and materials, are catalyzing large-scale investment in localized supply chains. In Canada, critical minerals strategies and cathode/anode projects are aligning with automaker commitments to EV production, while Mexico’s integration into regional assembly networks is unlocking new opportunities for localized pack and component manufacturing.

Market Challenges: Supply Chain Constraints, Qualification Bottlenecks, and Policy Uncertainty

Despite strong momentum, the North America electric vehicle battery components market faces structural and operational challenges that could constrain growth. Chief among these is the persistent reliance on imported critical minerals and midstream materials such as processed lithium, nickel, and graphite. While new projects are underway in the U.S. and Canada, the ramp-up of mining, refining, and processing capacity will take years, leaving the region exposed to price volatility and geopolitical risks.

Scale-up bottlenecks also represent a significant challenge. Equipment lead times for electrode processing, stamping, and casting can stretch to 18–24 months, while a shortage of skilled labor, particularly in advanced manufacturing, materials science, and quality control, risks slowing production schedules. Qualification requirements for automakers and regulatory compliance with evolving standards (e.g., UL, SAE, FMVSS updates) further lengthen development cycles, making time-to-market a key constraint for new entrants. Policy uncertainty compounds these challenges. While IRA and USMCA incentives are strong catalysts, future changes in political leadership or trade policy could alter credit eligibility, sourcing requirements, or tariff structures. This creates planning complexity for suppliers making multi-billion-dollar capital commitments.

Market Opportunities: Advanced Materials, Recycling, and Regional Integration

Despite these challenges, the market is rich with opportunities in North America electric vehicle battery components market. Lightweight and high-strength materials, such as aluminum, composites (GFRP, CFRP), and laminated busbars, are creating new avenues for differentiation in housings and interconnects. These innovations directly support automaker targets for range, safety, and cost competitiveness, while also enabling the transition to structural battery designs. Suppliers who invest early in these technologies can capture premium positions in the evolving value chain.

Recycling and resource recovery represent another major opportunity. The rapid scaling of gigafactories is creating a growing stream of manufacturing scrap and, eventually, end-of-life batteries. Facilities capable of recovering lithium, cobalt, nickel, and graphite will not only reduce environmental impact but also provide reliable secondary supply streams that help automakers meet IRA credit eligibility requirements. Companies integrating recycling into their operations can therefore secure long-term partnerships with OEMs and mitigate raw

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, “North America electric vehicle battery components market trajectory is structurally positive. Demand tailwinds such as EV adoption mandates, expanding commercial and off-road electrification, and sustained cost declines are durable. Technology is lifting performance (high-nickel and LFP roadmaps, silicon-rich anodes, pack integration) and raising the bar for thermal, dielectric, and structural design in housings and interconnects. Challenges still remain, dependence on imported critical minerals and midstream components is easing but not eliminated,; scale-up bottlenecks can elongate ramp curves,; and policy uncertainty introduces planning complexity. Even so, with the U.S. leading by volume, Canada accelerating materials and cell investments, and Mexico scaling pack/component assembly under USMCA, North America is converging on an integrated, competitive supply base through 2035.

North America Electric Vehicle Battery Components Market - A Regional Analysis

Focus on Vehicle Type, Battery Chemistry, Cell Format, Ecosystem Type, Component Type, Material Type, and Country Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

The North America electric vehicle battery components market offers high-growth opportunities fueled by policy incentives, supply-chain localization, and technology transitions. Key areas include the expansion of gigafactories and pack assembly plants across the U.S., Canada, and Mexico, investment in advanced housing materials and laminated busbar designs, and scaling of critical electrode materials such as lithium, nickel, cobalt, and graphite. The rapid shift toward cell-to-pack and structural battery designs is creating demand for new housings and interconnect technologies. In addition, the growth of commercial and off-road EV segments is amplifying component demand, while recycling and resource recovery are opening opportunities to secure secondary supply streams and align with IRA credit requirements.

To strengthen their position in the North America electric vehicle battery components market, leading suppliers are adopting several key strategies:

• Strategic Partnerships and OEM Collaborations: Firms are aligning with automakers and Tier 1 suppliers to co-develop housings, busbars, and electrode supply chains, ensuring compliance with IRA and USMCA requirements.

• Advanced R&D Investments: Significant funding is being directed toward next-generation electrode materials (e.g., silicon-rich anodes, high-nickel cathodes), lightweight housings, and laminated busbar designs to improve safety and efficiency.

• Capacity Expansion and Localization: Companies are establishing or expanding plants in the U.S., Canada, and Mexico to secure long-term supply contracts and qualify for domestic content credits.

• Mergers and Acquisitions: Suppliers are acquiring or partnering with recycling firms, cathode/anode developers, and midstream processors to integrate vertically and secure material access.

• Expansion into Emerging Segments: Players are targeting commercial fleets, heavy-duty trucks, and off-road vehicles, where larger battery packs and harsher duty cycles create outsized demand for housings, busbars, and electrode inputs.

A new entrant can gain a competitive edge by focusing on lightweight, high-strength housings (using aluminum or composites), innovative busbar materials (laminated or bimetal designs balancing cost and conductivity), and precision stamping for structural components. Investing in recycling and resource recovery capabilities can create synergies with OEM sustainability goals while supporting IRA credit compliance. Additionally, targeting commercial and off-road vehicle applications, segments with larger battery packs and higher per-vehicle content, offers a differentiated growth pathway. New companies that can prove qualification readiness, compliance documentation, and local production footprints will be best positioned to win contracts.

The USP of the North America electric vehicle battery components market report lies in its comprehensive coverage of the North America EV battery components market across six segmentation categories (vehicle type, chemistry, cell format, component, material, and country). It provides detailed insights into emerging technologies, supply-chain localization, and evolving pack architectures, supported by quantitative market forecasts through 2035. The report highlights how policy incentives, critical mineral strategies, and recycling integration are reshaping the competitive landscape. By linking market drivers, challenges, and opportunities with competitive benchmarking, the report equips stakeholders with actionable insights to make informed strategic and investment decisions.

The North America electric vehicle battery components market report is ideal for stakeholders across the EV value chain, including battery housing and busbar manufacturers, electrode material suppliers, pack assemblers, and Tier 1 integrators. Investors and venture capitalists seeking high-growth opportunities in EV supply chains will find strategic guidance. Policymakers and government agencies can leverage the analysis to align incentives and regulations with regional supply-chain development. Finally, automakers, research institutions, and consulting firms focused on EV strategy, supply-chain localization, and materials innovation will benefit from the report’s deep dive into trends, forecasts, and competitive strategies.