A quick peek into the report

Global Intelligence, Surveillance, and Reconnaissance (ISR) Aircraft and Drones Market Overview

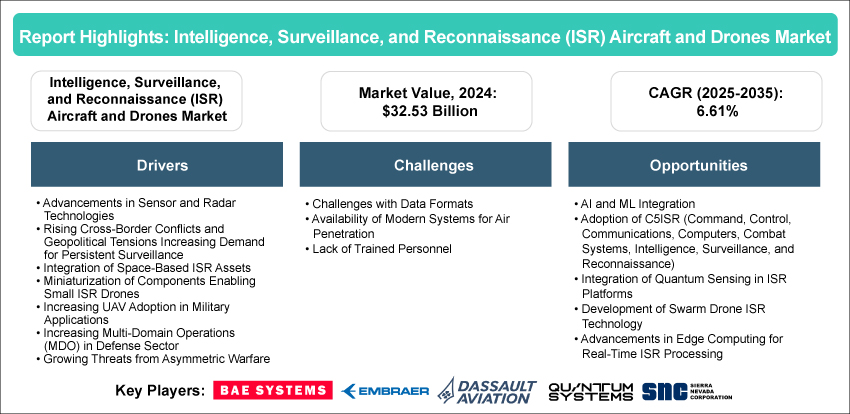

The global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market was valued at $32.53 billion in 2024 and is projected to reach $65.45 billion by 2035, growing at a CAGR of 6.61%. The market is propelled by advancements in sensor and radar technologies, increasing adoption of AI and machine learning, and rising demand for real-time situational awareness across defense, homeland security, and border monitoring applications. Collaborations between OEMs, technology integrators, and defense agencies are further accelerating innovation in compact, multi-mission ISR platforms, thereby supporting the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market growth.

Introduction of ISR Aircraft and Drones

ISR aircraft and drones are specialized platforms designed to gather intelligence, perform surveillance, and conduct reconnaissance missions across air, maritime, and land domains. These systems integrate electro-optical/infrared (EO/IR) sensors, radar, signals intelligence (SIGINT), and communications equipment to detect, track, and analyze targets. They are increasingly critical for military operations, border security, disaster management, and maritime patrol, offering persistent situational awareness while minimizing risk to human operators.

Market Introduction

The global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market has been evolving rapidly due to the convergence of advanced sensors, AI-enabled analytics, and unmanned aerial technologies. Developments in AESA radar, deep sensing, swarm drones, and edge computing are enhancing detection, target identification, and autonomous operations. Rising geopolitical tensions, modernization of armed forces, and strategic defense investments are fueling demand for next-generation ISR solutions capable of operating in contested or denied airspace. These technological advancements are redefining the ISR landscape, enabling more precise, rapid, and cost-effective intelligence collection.

Industrial Impact

The global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market has a wide-ranging industrial impact across defense manufacturing, technology development, and security operations. Advancements in ISR platforms, including AI-enabled analytics, multi-sensor integration, and autonomous capabilities, drive innovation and enhance operational efficiency for military, homeland security, and border surveillance applications. This growth encourages collaborations between defense OEMs, technology integrators, and research institutions, elevating production standards and fostering R&D in advanced sensors, radar systems, and unmanned aerial technologies. Moreover, increasing investments in ISR solutions contribute to workforce expansion in aerospace engineering, software development, and electronics integration.

Key players operating in the global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market include Northrop Grumman Corporation, Lockheed Martin Corporation, General Atomics Aeronautical Systems, BAE Systems, L3Harris Technologies, Leonardo S.p.A., Elbit Systems Ltd., Thales Group, Raytheon Technologies Corporation, AeroVironment, Inc., Boeing, Dassault Aviation, Bombardier, and Sierra Nevada Corporation. These companies focus on strategic partnerships, technology collaborations, and acquisitions to expand their ISR capabilities, enhance multi-mission platforms, and strengthen their global market presence.

Market Segmentation:

Segmentation 1: by End-Use Industry

• Reconnaissance and Surveillance

• Electronic Warfare

• Search and Rescue Operations

• Airborne Early Warning Capabilities

• Maritime Support/Patrol

• Tactical Operations

• Target Acquisition

Reconnaissance and Surveillance Segment to Dominate the Global Intelligence, Surveillance, and Reconnaissance (ISR) Aircraft and Drones Market (by End-Use Industry)

The reconnaissance and surveillance segment dominates the global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market, as they are critical for situational awareness, threat detection, and strategic decision-making. Defense forces and government agencies prioritize aerial ISR for battlefield intelligence, maritime domain awareness, and border monitoring. High-altitude long-endurance (HALE) UAVs and manned ISR aircraft are increasingly equipped with AI-driven analytics, electro-optical/infrared (EO/IR) sensors, and synthetic aperture radar (SAR) to improve target detection and accuracy. For example, in 2024, Northrop Grumman continued Global Hawk contracts to support extended reconnaissance missions.

From a commercial perspective, investments in ISR technologies have surged, with collaborations between defense contractors and technology firms focusing on sensor fusion, AI-based processing, and autonomous operations. For instance, in May 2024, Anduril Industries received U.S. Department of Defense funding to expand its autonomous ISR drone programs with edge computing capabilities, while Elbit Systems partnered with Adani Defense to produce ISR drones for border security. Geopolitical tensions and rising defense budgets in NATO, Indo-Pacific, and Middle Eastern regions are further driving demand for persistent, all-weather ISR solutions. Consequently, the reconnaissance and surveillance segment maintains the largest market share due to its indispensable value in both peacetime operations and conflict scenarios.

Segmentation 2: by Platform

• Military Aircraft

o Fighter Jets

o Special Mission Aircraft

o Missionized Business Jets

o Military Transport Aircraft

• Military Drones

o Medium-Altitude Long Endurance (MALE) Drones

o High-Altitude Long Endurance (HALE) Drones

o Small Drones

o Military Helicopter

Military Aircraft to Dominate the Global Intelligence, Surveillance, and Reconnaissance (ISR) Aircraft and Drones Market (by Platform)

Military aircraft continue to lead the global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market due to their unmatched endurance, payload capacity, and operational versatility. Platforms such as the Boeing P-8A Poseidon, Lockheed Martin U-2S, and Bombardier Global 6500-based ISR variants provide high-altitude, long-range surveillance with integrated SIGINT, COMINT, and ELINT suites. These aircraft support maritime patrol, battlefield reconnaissance, and strategic intelligence missions. Their ability to host extensive sensor arrays, onboard analysts, and real-time data links makes them critical for multi-domain awareness, particularly in complex regions like the Indo-Pacific and Eastern Europe.

Recent investments underscore this dominance. For instance, in April 2024, the U.S. Navy approved a $1.3 billion extension for additional P-8A Poseidon aircraft. The U.K. RAF upgraded its Rivet Joint fleet with next-generation electronic warfare systems, and India expanded its ISR capabilities by inducting Dassault Falcon 2000 platforms with indigenous sensor payloads. While unmanned ISR drones are growing in popularity due to flexible deployment and lower operational costs, manned platforms remain indispensable for missions requiring secure data handling, crew adaptability, and extended flight durations, especially in contested airspace. All this further drives the demand for intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market over the forecast timeframe from 2025 to 2035.

Segmentation 3: by Component Type

• Surveillance System

o Light Detection and Ranging (LiDAR)

o Electro-Optical/Infrared Sensor (EO/IR Sensors)

o Radar

o Others

• Communication System

o SATCOM

o Antenna

o Datalinks

• Signal Intelligence (SIGINT) System

o Electronic Intelligence (ELINT)

o Communication Intelligence (COMINT)

• Software

o Mission Management

o Threat Detection

• Others

Surveillance System to Lead the Global Intelligence, Surveillance, and Reconnaissance (ISR) Aircraft and Drones Market (by Component Type)

Surveillance systems, encompassing radar, EO/IR sensors, and LiDAR, continue to dominate the global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market. In 2024, these systems accounted for the largest component share, driven by their critical role in real-time target acquisition, high-resolution imaging, and wide-area situational awareness. Unlike SIGINT modules, communication systems, or software, which often require integration with other platforms, surveillance payloads deliver immediate, mission-critical intelligence from deployment. High-altitude manned aircraft further amplify these capabilities with extended endurance and larger payload capacities, supporting operations such as border security, maritime patrol, and strategic reconnaissance.

Industry players in the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market are enhancing surveillance systems with next-generation technologies. Boeing, Bombardier, and Embraer are integrating advanced radar, multi-spectral imaging, LiDAR, and synthetic aperture radar to meet evolving defense and homeland security requirements. Concurrently, traditional manned ISR platforms are upgrading EO/IR and radar suites for improved detection and precision. This persistent focus on advanced surveillance capabilities underscores their status as the primary growth driver in the ISR aircraft and drones market, while communication systems, SIGINT platforms, and software remain supportive components.

Segmentation 4: by Support Service

• Simulation

• Active Maintenance

• Data Analytics and Post-Processing

Segmentation 5: by Region

• North America: U.S., Canada, and Mexico

• Europe: Germany, France, U.K., Russia, and Rest-of-Europe

• Asia-Pacific: China, Japan, South Korea, India, Australia, and Rest-of-Asia-Pacific

• Rest-of-the-World: Latin America and the Middle East and Africa

North America is expected to maintain a leading position in the global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market, holding the largest market share throughout the forecast period. This dominance is supported by the presence of established defense aerospace companies, advanced technological infrastructure, and increasing defense budgets in the U.S. and Canada. Strong government initiatives for modernizing ISR fleets, coupled with ongoing investments in AI-driven sensors, electronic warfare suites, and autonomous drones, are driving demand. Additionally, North America’s leadership in defense R&D and its strategic focus on multi-domain intelligence operations reinforce its market position, while collaborations between defense contractors and technology firms accelerate the deployment of advanced ISR platforms across military and homeland security applications.

Asia-Pacific intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market, emerging as a significant growth region, lags North America in terms of technological maturity and defense spending, though rapid industrialization, rising defense investments, and increasing adoption of UAVs and ISR aircraft in countries like China, India, Japan, and Australia are expected to drive growth in the coming decade.

Demand - Drivers, Limitations, and Opportunities

Market Demand Driver: Advancements in Sensor and Radar Technologies

One of the most significant drivers in the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market is the rapid progress in sensor and radar systems. Modern radars, including active electronically scanned array (AESA) designs, now offer higher resolution, extended range, and multi-band capabilities, enabling precise target detection and tracking. Electro-optical/infrared (EO/IR) sensors have become lighter and more efficient, delivering sharper imagery from smaller platforms. Companies such as BAE Systems and Elbit Systems have introduced compact AESA radars for unmanned aerial vehicles (UAVs), while L3Harris Technologies launched an ISR suite integrating radar feeds, EO/IR imagery, and signals intelligence into a unified platform. Sensor fusion, software-defined architectures, and modular upgrades are enhancing long-term platform viability and operational efficiency. Military and homeland security stakeholders increasingly recognize the value of real-time situational awareness, driving investment in next-generation ISR sensors and radar technologies.

Market Challenge: Availability of Modern Systems for Air Penetration

A major restraint in the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market is the limited availability of platforms capable of operating in contested or denied airspace. While many drones and reconnaissance aircraft perform effectively in permissive environments, they often lack stealth features, high-speed capabilities, or advanced electronic countermeasures needed to evade sophisticated air defenses. Legacy ISR platforms may be vulnerable against near-peer adversaries such as China or Russia, and next-generation stealth drones or penetrating ISR jets remain restricted due to classification, export controls, or early-stage development. Programs such as the Northrop Grumman stealth drone projects and the European Future Combat Air System (FCAS) are still in developmental phases, delaying widespread availability. As a result, militaries may rely on retrofitted electronic self-protection suites, which can mitigate but not fully overcome high-threat vulnerabilities, thereby constraining high-end ISR platform adoption and market expansion.

Market Opportunity: AI and ML Integration

Integrating artificial intelligence (AI) and machine learning (ML) into ISR platforms presents a transformative opportunity for the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market. Advanced algorithms automate image recognition, signal analysis, and target identification, reducing analyst workload and accelerating decision cycles. Leonardo DRS incorporates AI-driven threat detection in full-motion video to flag anomalies, while L3Harris Technologies’ real-time ML processing classifies objects and alerts command centres to unusual activity. AI also enables autonomy, with General Atomics testing “AI co-pilot” functionality for the MQ-9 Reaper and Elbit Systems improving swarm drone reliability. Implementation challenges, including onboard processing requirements and secure data links, are being addressed by companies such as AeroVironment and Raytheon Technologies. AI and ML integration enhances mission effectiveness across tactical drones, maritime patrol aircraft, and large ISR platforms, creating a high-growth segment in the coming decade.

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, “The global intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market is set for strong growth, driven by advancements in sensors, radar, AI/ML, and edge computing. Rising defense budgets, demand for real-time situational awareness, and adoption of C5ISR and quantum sensing are fuelling investments across manned and unmanned ISR platforms. Key players, including L3Harris Technologies, General Atomics, Elbit Systems, and Raytheon Technologies, focus on sensor fusion, software-defined architectures, and AI-enabled processing to enhance mission effectiveness and platform longevity. While stealth ISR aircraft remain limited, retrofitted and upgraded systems continue to expand market opportunities worldwide.”

Intelligence, Surveillance, and Reconnaissance (ISR) Aircraft and Drones Market - A Global and Regional Analysis

Focus on End-Use Industry, Platform, Component, and Country-Level Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

Intelligence, surveillance, and reconnaissance (ISR) aircraft and drones are specialized platforms designed to collect real-time intelligence through aerial monitoring, data acquisition, and persistent situational awareness. These systems leverage advanced sensors, high-resolution imaging, signal intelligence (SIGINT), radar, and communications payloads to support military, homeland security, border surveillance, disaster response, and critical infrastructure monitoring. With rising defence modernization, increased geopolitical tensions, and rapid advancements in autonomous systems and AI-driven analytics, ISR aircraft and drones have become essential for mission planning, threat detection, and strategic decision-making across air, land, and maritime domains.

Significant opportunities include the integration of artificial intelligence (AI) and machine learning (ML) for autonomous decision-making, widespread adoption of C5ISR frameworks, the emergence of quantum-enabled sensing technologies, the development of swarm-drone ISR capabilities, and advancements in edge computing for real-time on-platform processing. These innovations are driving next-generation ISR modernization across defense, homeland security, and commercial sectors.

Leading companies are adopting collaborative strategies, including joint ventures, technology partnerships, and multi-domain integration programs to enhance payload performance, expand operational ranges, and accelerate AI-enabled mission capabilities. Strategic alliances with defense ministries, aerospace OEMs, and sensor technology providers help companies access new markets, enhance platform interoperability, and secure long-term modernization contracts.

New entrants in the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market should prioritize partnerships with established ISR platform manufacturers, focus on developing advanced sensor payloads, AI-enabled analytics, secure communication systems, and niche ISR capabilities such as swarm autonomy or edge-processing modules. Additionally, securing funding for R&D, building strong integration capabilities, and establishing robust distribution and after-sales networks will help maintain competitiveness.

The following are some of the USPs of the intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market report:

• A dedicated section analyzing trends adopted by leading ISR aircraft and drone manufacturers

• Comprehensive competitive landscape mapping of the global ISR ecosystem

• Detailed qualitative and quantitative insights at regional and country levels, with segmentation by platform, application, and payload type

• In-depth supply chain and value chain analysis

• Exclusive defense budget analysis for each country covered in the scope, supporting procurement forecasting and capability-development assessments

The intelligence, surveillance, and reconnaissance (ISR) aircraft and drones market report is highly valuable for ISR aircraft and drone manufacturers, defense contractors, payload and sensor suppliers, aerospace OEMs, national defense agencies, border-security authorities, system integrators, and investors evaluating opportunities in next-generation ISR technologies.