A quick peek into the report

Factory-of-the-Future Mobility Solutions Market Overview

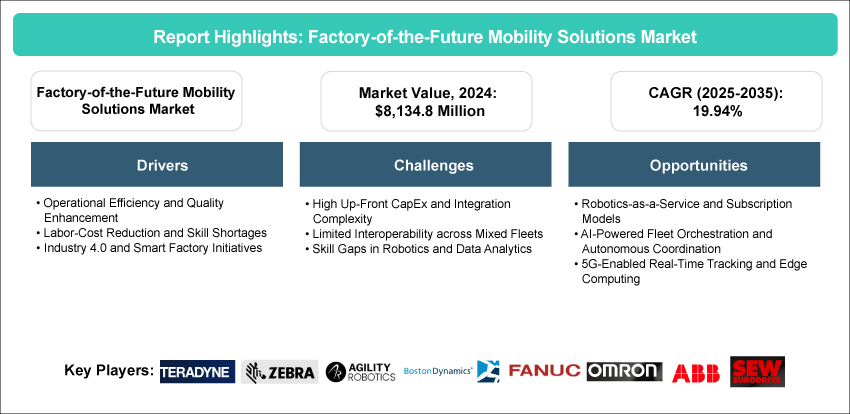

The factory-of-the-future mobility solutions market was valued at $8,134.8 million in 2024 and is projected to grow at a CAGR of 19.94%, reaching $58,681.4 million by 2035. The factory-of-the-future mobility solutions market landscape is being shaped by several decisive trends. Autonomy capabilities are advancing rapidly, with vision-based navigation, semantic mapping, and AI-enabled path planning enabling equipment to operate reliably in dynamic, less-structured environments. Interoperability is improving, driven by frameworks such as VDA-5050 and ISO 3691-4, allowing seamless mixed-fleet orchestration of AMRs, AGVs, automated forklifts, and cobots under unified management platforms. Digital twin deployment is shortening commissioning cycles, enabling layout validation and performance optimization in days rather than weeks. Commercially, automation-as-a-service and output-linked pricing models are lowering adoption barriers and aligning investment with operational performance.

From a compliance and safety standpoint, integration of collision-avoidance systems, proximity detection, and adherence to collaborative operation standards (such as ISO/TS 15066) is accelerating regulatory clearance and even unlocking insurance benefits. Structurally, labor constraints and the need for throughput stability are reinforcing automation investment, with e-commerce, semiconductor, and EV manufacturing as priority verticals.

Introduction of Factory-of-the-Future Mobility Solutions Market

The study conducted by BIS Research highlights factory-of-the-future mobility solutions as a structural reset driven by electrification, automation, digital manufacturing, and sustainability mandates. Traditional automotive production models, linear, asset-heavy, and forecast-driven, are increasingly misaligned with a market that now demands speed, customization, resilience, and lower carbon intensity. This shift has accelerated the emergence of the Factory-of-the-Future (FoF), a highly connected, intelligent, and adaptive manufacturing paradigm purpose-built for next-generation mobility solutions. In addition, Mobility-as-a-Service (MaaS) in the factory-of-the-future mobility solutions market enables manufacturers to shift from asset-heavy, fixed automation investments to usage-based, software-orchestrated mobility solutions, allowing intralogistics fleets, autonomous systems, and robotics to scale on demand while improving capital efficiency, flexibility, and time-to-value.

Market Introduction

The factory-of-the-future mobility solutions market represents a convergence of advanced manufacturing technologies, data-driven decision-making, and human-centric design. It is not a single factory blueprint, but a modular, scalable operating model that integrates cyber-physical systems across the value chain from design and engineering to production, logistics, and after-sales support. The Factory-of-the-Future is not an optional innovation; it is a strategic response to market volatility. Battery supply constraints, semiconductor shortages, and regionalized production policies have exposed the fragility of legacy manufacturing models. FoF architectures enable resilient, localized, and demand-responsive production, allowing mobility players to pivot faster across powertrains, platforms, and markets. An effective analogy is content flow optimization; just as high-performing digital content adapts to user intent and channel performance, FoF-enabled factories dynamically rebalance capacity, labor, and resources based on real-time signals, maximizing relevance, efficiency, and return on investment.

Industrial Impact

The factory-of-the-future mobility solutions market has been producing measurable, systemic impact across the mobility manufacturing landscape. Its influence extends beyond incremental efficiency gains, fundamentally reshaping how mobility products are designed, produced, scaled, and sustained across their lifecycle. The industrial impact can be assessed across five interrelated dimensions, namely, productivity, flexibility, cost structure, sustainability, and ecosystem resilience.

Market Segmentation:

Segmentation 1: by Vehicle Type

• Autonomous Mobile Robots (AMRs)

• Automated Forklifts

• Automated Guided Vehicles

• Cobots

• Others

Automated Guided Vehicles to Dominate the Factory-of-the-Future Mobility Solutions Market (by Vehicle Type)

Automated guided vehicles (AGVs) are positioned to dominate the factory-of-the-future mobility solutions market landscape due to their alignment with the structural realities of modern mobility manufacturing. Automotive and EV plants operate on highly predictable, high-frequency material flows, line feeding, pallet transfer, battery pack movement, and body-in-white logistics, where repeatability, safety, and uptime outweigh the need for navigation freedom. AGVs excel in these deterministic environments, particularly for heavy payloads exceeding 1-2 tons, where guided paths reduce collision risk and ensure process stability. Industry benchmarks indicate that AGV-led intralogistics can improve material-handling efficiency by 20-30% while reducing internal logistics labor costs by up to 40%. Much like a well-orchestrated content distribution engine that prioritizes consistency and reliability over experimentation, AGVs form the operational backbone of smart factories, providing stable, scalable, and cost-efficient material flow that supports high-volume production, regulatory compliance, and zero-defect manufacturing objectives in next-generation mobility plants.

Segmentation 2: by Solution Type

• Software Platform

• Hardware

• Services

Software Platform to Dominate the Factory-of-the-Future Mobility Solutions Market (by Solution Type)

Software platforms are set to dominate the factory-of-the-future mobility solutions market as manufacturing value increasingly shifts from physical assets to digital intelligence. In advanced mobility plants, competitive advantage no longer comes from individual machines, but from the software layer that orchestrates them, integrating MES, MOM, digital twins, AI analytics, and industrial IoT into a single decision-making backbone.

Segmentation 3: by Deployment Model

• On-Premise License

• Mobility-as-a-Service (MaaS)

On-Premises License to Dominate the Factory-of-the-Future Mobility Solutions Market (by Deployment Model)

On-premises licensing is expected to dominate the factory-of-the-future mobility solutions market by deployment method, primarily due to the sector’s stringent requirements around data sovereignty, latency control, and operational resilience. Mobility manufacturing environments generate high-frequency, mission-critical data, robot coordination, safety systems, quality inspection, and battery traceability that cannot tolerate network dependency or downtime.

Segmentation 4: by Region

• North America: U.S., Canada, and Mexico

• Europe: Germany, U.K., France, Italy, and Rest-of-Europe

• Asia-Pacific: China, Japan, India, South Korea, and Rest-of-Asia-Pacific

• Rest-of-the-World: South America and the Middle East and Africa

Currently, Europe is considerably growing in the factory-of-the-future mobility solutions market, with Germany at the forefront of this advancement. Germany also retains a deep mobility production base, with roughly 4.1 million passenger cars manufactured domestically in 2024 and a dense network of suppliers and assembly sites, conditions that accelerate the adoption of factory digitization to protect quality, speed, and competitiveness. On the automation side, Germany is among the global leaders in industrial robotics intensity (robot density around ~429 robots per 10,000 employees, per IFR), reinforcing its readiness to scale AI-enabled inspection, robotics, and connected operations across mobility plants. Finally, Germany’s institutional leadership in Industrie 4.0, supported through national initiatives focused on smart, digital production, creates a policy and standards tailwind that makes Germany the most structurally advantaged market for FoF mobility deployment in Europe.

Demand - Drivers, Limitations, and Opportunities

Market Demand Drivers: Operational Efficiency and Quality Enhancement

One of the primary drivers for robotics adoption is the pursuit of higher operational efficiency and superior product quality. Automated systems and robots can work with precision and consistency beyond human capability, leading to increased throughput and reduced error rates. By eliminating human errors and variability, companies significantly improve quality control; a recent industry survey found that 40% of manufacturers now prioritize adopting robots specifically to enhance quality. Robots can operate 24/7 without fatigue, ensuring consistent performance that boosts productivity while maintaining high-quality standards. This dual benefit of greater efficiency and improved quality makes a compelling case for investment in robotics, as it streamlines operations and reduces waste from defects or rework.

Market Challenges: High Up-Front CapEx and Integration Complexity

Despite its long-term benefits, robotics adoption comes with significant challenges, foremost among them the high initial capital expenditure and the complexity of integration. Industrial robots and automation systems often require a large up-front investment, which is needed for purchasing the robots, retrofitting facilities, and deploying new infrastructure, which can be a barrier, especially for small and mid-sized firms. Justifying the ROI can be difficult when the payback period is uncertain, and many companies find it challenging to justify the cost of robot installation at the outset. In addition, integrating robotics into existing operations is a complex task. Factories and warehouses must ensure new robots can communicate with legacy equipment, enterprise software, and each other. This often involves custom engineering, system integration work, and potential downtime during installation. The complexity of integration with existing systems is a common hurdle, requiring specialized expertise and careful planning to avoid disruptions. Companies may need to reconfigure floor layouts, upgrade power supplies or network infrastructure, and modify workflows to accommodate robots, all of which add to the implementation challenge. These factors make the adoption process daunting, as organizations must weigh the substantial initial costs and technical complexity against the future efficiency gains.

Market Opportunities: Robotics-as-a-Service and Subscription Models

Emerging business models like robotics-as-a-service (RaaS) present a promising opportunity to accelerate the factory-of-future mobility solutions market growth by lowering adoption barriers. Instead of purchasing robots outright (with large capital expenditure), companies can subscribe to robotic solutions on a pay-as-you-go or lease basis, effectively turning robotics into an operational expense. This model offers a cost-effective solution for companies to implement automation, with much lower upfront costs and faster ROI compared to the traditional approach of buying equipment.

For example, a manufacturer might pay a monthly fee or a usage-based rate (e.g., per hour or per pick) for a fleet of warehouse robots, which is often more budget-friendly than spending hundreds of thousands of dollars at once. RaaS providers typically handle installation, maintenance, and software updates as part of the service, reducing the technical burden on end users. The opportunity here is twofold: for customers, RaaS provides flexibility and scalability (they can start small and scale up automation as needed, or scale down during off-peak seasons), and for robotics vendors, it opens up a larger addressable market (including small and mid-sized businesses that previously couldn’t afford automation). This subscription-based trend aligns with the broader shift toward X-as-a-Service models in technology. As awareness grows, RaaS is expected to democratize access to robotics by mitigating the high CapEx challenge, much like cloud computing services did for IT infrastructure. In the coming years, more solution providers are likely to offer subscription models or leasing options, making robotics adoption more accessible and driving further market expansion.

Analyst View

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, “the factory-of-the-future mobility solutions market is entering a scale-up phase, where value is shifting from isolated automation projects to platform-led operating models. BMW’s decision to industrialize and roll out its Virtual Factory across 30+ sites, with a stated target of up to 30% lower production-planning costs, signals that digital twins are becoming a core enterprise capability rather than a pilot tool, especially ahead of multiple vehicle launches and factory changeovers. Leaders are standardizing on digital twins, AI-enabled manufacturing platforms, and partner ecosystems to convert smart factory investment into repeatable, multi-plant performance improvements, moving the market from “technology adoption” to “industrial operating advantage.”

Factory-of-the-Future Mobility Solutions Market - A Global and Regional Analysis

Focus on End-Use Industry, Vehicle Type, Solution Type, Deployment Model, and Country Level Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

Factory-of-the-future mobility solutions refer to an advanced manufacturing paradigm designed specifically to support the production of next-generation mobility products, electric vehicles (EVs), autonomous systems, connected vehicles, and emerging mobility platforms, through digitally integrated, intelligent, and sustainable factories. It represents a shift from traditional, linear automotive manufacturing to software-orchestrated, data-driven, and highly flexible production ecosystems.

The factory-of-the-future mobility solutions market presents multiple high-value business opportunities as OEMs and suppliers modernize production to support EVs, autonomous systems, and software-defined vehicles. These opportunities span technology, services, and ecosystems, with strong recurring-revenue potential and long-term strategic relevance.

To strengthen their market position in the factory-of-the-future mobility solutions industry, existing players have been adopting several strategic initiatives:

• Strategic Partnerships and Collaborations: Existing players in the factory-of-the-future mobility solutions industry are increasingly adopting strategic, system-level approaches to defend and expand their market positions as competition intensifies and technology cycles accelerate. Rather than competing solely on hardware or isolated solutions, incumbents are repositioning themselves as platform owners, ecosystem orchestrators, and long-term transformation partners.

• Integration of MES/MOM: One major strategy is the shift toward platform consolidation and standardization. Leading players are integrating MES/MOM, digital twins, intralogistics control, AI analytics, and quality management into unified platforms that can be replicated across multiple plants. This approach increases customer lock-in and raises switching costs, with analysts estimating that standardized, multi-plant deployments can improve share-of-wallet by 20-40%. The strategy resembles a content hub model, where controlling the central platform ensures consistent engagement and long-term relevance.

• Ecosystem-Based Co-Innovation: Market leaders are also deepening their positions through ecosystem-based co-innovation. Rather than building everything in-house, companies are forming structured partnerships with robotics vendors, AI startups, cloud and edge providers, and system integrators. With more than 60% of large FoF projects now involving multi-vendor stacks, incumbents that act as ecosystem coordinators gain strategic control over complex deployments and improve win rates on large transformation contracts.

For a new company entering the factory-of-the-future mobility solutions market, competing head-on with established OEMs and large automation vendors is neither practical nor necessary. The most effective path to differentiation lies in targeting high-growth, underserved, and software-led value pools where incumbents are slower to innovate.

The primary USP of this report lies in its mobility-first, factory-of-the-future lens, which moves beyond generic Industry 4.0 analysis to deliver actionable, decision-ready insights tailored specifically to next-generation mobility manufacturing. Unlike conventional market reports that focus on technology inventories or high-level trends, this study integrates market data, competitive strategy, and operational impact into a single, cohesive narrative aligned with real factory transformation journeys.

This report is designed for decision-makers and strategy leaders who need to translate factory-of-the-future ambition into clear investment, technology, and competitive choices within the mobility manufacturing ecosystem. It is especially valuable for stakeholders who operate at the intersection of operations, digital transformation, and long-term growth strategy.