A quick peek into the report

Airborne Laser Terminal Market Overview

Introduction of the Airborne Laser Terminal Market

The airborne laser terminal market focuses exclusively on high-speed optical communication solutions designed for airborne platforms, representing a rapidly evolving segment in aerospace and communications. Since its inception, the market has been supported by significant research and development efforts, with early demonstrations starting in 2019 through NASA’s Airborne Laser Communication Testbed. This initiative, which accumulated over 50 flight hours on aircraft like the PC-12 and DHC-6 Twin Otter, successfully validated gigabit-class air-to-ground and air-to-air optical communication links under real-world turbulence, marking a key milestone in the feasibility of optical communication for airborne platforms.

Commercial progress followed with Mynaric’s introduction of the HAWK terminal in 2022, designed for aircraft and UAVs. However, production was paused due to technical challenges, signalling the complexities involved in scaling this technology. Despite these hurdles, the airborne laser terminal market continues to be driven by government and defense sector funding, primarily focused on prototype testing and development. As the market progresses, adoption is expected to moderate post-2026, with a transition toward commercial applications, particularly in UAV-based delivery networks and broadband services for airlines. These developments mark the beginning of the airborne laser terminal market's move into its early commercial phase by 2028, as the technology matures and becomes more widely adopted across various sectors.

Market Overview

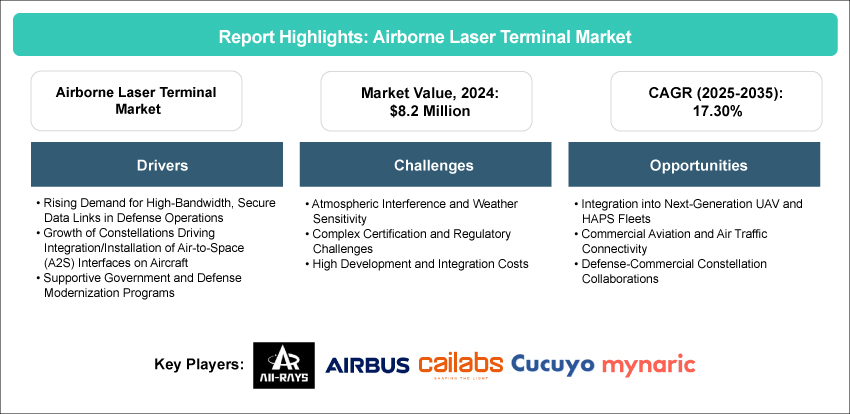

The global airborne laser terminal market, valued at $8.2 million in 2024, is positioned for substantial growth, with an anticipated CAGR of 17.30% from 2025 to 2035, reaching $44.7 million by 2035. This robust growth is primarily driven by the increasing demand for secure, high-speed communication systems across various sectors, particularly government and defense applications. Among applications, the Government and Defense segment is the fastest growing, as these sectors require reliable, jam-resistant communication solutions for military operations, surveillance, and reconnaissance. In terms of product segmentation, Air-to-Space terminals are witnessing the fastest growth within the airborne laser terminal market, driven by advancements in space-to-air optical communication. Regionally, North America’s market dominates, with the U.S. leading the way through substantial investments in defense and aerospace programs that prioritize airborne laser terminal technologies. These developments are positioning the airborne laser terminal market as a key player in global communication infrastructure, fostering further innovation and commercial adoption.

Industrial Impact

The airborne laser terminal market has been making a significant impact across the aerospace, defense, and telecommunications sectors by transforming high-speed, secure communication systems. As the demand for secure, resilient communication solutions grows, the airborne laser terminal market is driving innovations in optical communication technologies, particularly in jam-resistant systems for contested environments. This shift is creating valuable opportunities for technology providers, system integrators, and defense contractors, prompting collaboration across aerospace companies and commercial entities. The growing demand for air-to-ground, air-to-air, and air-to-space laser communication systems is fostering advancements in optical subsystems, turbulence mitigation, and hybrid RF/FSO designs within the airborne laser terminal market. Additionally, the push for standardized optical communication protocols is reducing integration risks and enhancing market accessibility, allowing seamless connectivity with space-based networks. These technological advancements are not only enhancing military communications but also unlocking commercial applications, such as UAV-based networks and in-flight broadband services. Overall, the airborne laser terminal market is contributing to both economic growth and technological progress, solidifying its role in the global communications infrastructure.

Market Segmentation:

Segmentation 1: By End User

• Government and Defense

• Commercial

Government and Defense to Lead the Market as the Fastest-Growing End-User Segment (by Application)

The government and defense sectors are expected to drive the fastest growth in the airborne laser terminal market, as they have the most pressing need for high-capacity, resilient communication links in congested and contested electromagnetic environments. With the U.S. Department of Defense's Electromagnetic Spectrum Superiority Strategy highlighting growing risks in RF, there is a clear push toward alternatives offering lower detection probabilities and stronger resistance to jamming, traits inherent to airborne laser communication (lasercom). Mission-critical applications such as ISR backhaul, command and control in contested environments, and emissions control align perfectly with the benefits Lasercom provides. Additionally, defense space architectures are standardizing around optical interoperability, with the Space Development Agency's Optical Communications Terminal (OCT) standard v4.0.0 enabling space-to-air links. Government-funded demos, like NASA Glenn’s Airborne Laser Communication Testbed, have demonstrated the operational viability of lasercom in real turbulence, validating its use in aircraft. These advancements, alongside ongoing defense funding, are accelerating market growth and adoption.

Segmentation 2: By Solution

• Air-to-Space

• Air-to-Air

• Air-to-Ground

Segmentation 3: By Component

• Optical Assembly and Subsystems

• Electronics and Signal Processing

• Mechanical and Casing Structure

• Others

Segmentation 4: By Platform

• Aircraft

• Unmanned Aerial Vehicles (UAVs)

• Helicopters

Segmentation 5: By Region

• North America

• Europe

• Asia-Pacific

• Rest-of-the-World

Recent Developments in the Airborne Laser Terminal Market

• In 2025, General Atomics Electromagnetic Systems (GA-EMS) and Kepler Communications successfully demonstrated a two-way optical communication link between an aircraft and a low Earth orbit (LEO) satellite. Using GA-EMS’ Optical Communications Terminal (OCT) integrated in a 12-inch LAC-12 turret, the system maintained a stable connection during flight, proving the viability of SDA-compatible standards for air-to-space data exchange. This breakthrough achievement has placed the technology at TRL 8–9, indicating its near deployment readiness for defense architectures.

• Since 2023, the U.S. Naval Research Laboratory (NRL) has operated a sophisticated testbed to validate optical terminal interoperability built to Space Development Agency (SDA) standards. Simulating orbital conditions, the testbed ensures multi-vendor compatibility for communication across SDA’s proliferated LEO constellations and future air-to-space platforms. The system, now at TRL 8, plays a critical role in establishing reliable procurement processes and technical validation across contractors for scalable airborne and satellite laser networks.

• In 2025, the U.S. Space Systems Command’s Enterprise Space Terminal (EST) Phase-2 initiative selected CACI, General Atomics, and Viasat to develop low-SWaP-C, interoperable optical terminals. These prototypes aim to implement enterprise waveform standards for crosslink and space-to-air connectivity, aligning with the Space Development Agency’s OCT v4.0 framework. By reaching TRL 8–9 maturity, the program establishes interoperability as a procurement standard, facilitating large-scale deployment across defense and commercial domains.

• In 2024, Cucuyo partnered with Cavok UAS to test the P-100 installed on Cavok drones. Following successful flight trials in 2025, this collaboration has demonstrated the technical maturity and real-world applicability of Cayuco’s airborne laser terminal systems.

• In 2023, Airbus and VDL Group began a strategic collaboration to develop and industrialize the UltraAir terminal. The partnership, which includes Airbus designing the system and VDL manufacturing critical components, aims to advance military communications. By 2025, flight testing of the UltraAir terminal will further demonstrate its capabilities in military applications.

• In 2023, Aalyria announced a partnership with Airbus to explore the feasibility of ultra-high-speed optical networks, enhancing connectivity between aircraft, spacecraft, and terrestrial fiber networks. This collaboration will push the boundaries of air-to-ground and air-to-air optical communication, positioning Aalyria at the forefront of next-generation communication technologies.

Analyst’s Thoughts

According to Dhrubajyoti Narayan, Principal Analyst at BIS Research, “The global airborne laser terminal market has been experiencing rapid growth, driven primarily by increasing demand for secure, high-speed optical communication systems in government and defense sectors. As the need for resilient, jam-resistant, and high-capacity communication links grows, especially in contested environments, air-to-air, air-to-ground, and air-to-space technologies are emerging as essential solutions. The government and defense sectors, with their focus on secure and efficient communication for military operations, surveillance, and reconnaissance, are expected to witness the fastest growth. This shift is largely driven by advancements in optical beam technologies, turbulence mitigation, and ongoing investments in prototype testing and military-grade systems. North America is expected to lead the market due to its well-established aerospace and defense infrastructure, coupled with significant government funding for defense programs and technological development. The U.S. government is advancing air-to-space optical communication systems through agencies like NASA and the Space Development Agency, making North America the primary region for ALT deployment and innovation.

Despite these advancements, challenges such as high development costs, complex regulatory frameworks, and integration hurdles remain key obstacles for broader market penetration, especially for commercial applications. However, with increasing standardization, successful flight trials, and government partnerships, the market is expected to evolve rapidly, opening opportunities for both defense and commercial applications in the near future.”

Airborne Laser Terminal Market - A Global and Regional Analysis

Focus on Application, Product, and Regional Analysis - Analysis and Forecast, 2025-2035

Frequently Asked Questions

Airborne laser terminal technology refers to advanced optical communication systems that enable high-speed, secure data transfer between aircraft, ground stations, or space-based assets using laser beams. These systems leverage tightly collimated optical beams to provide a more reliable, jam-resistant alternative to traditional radio frequency (RF) communications, offering enhanced capacity and a lower probability of interception.

For government and defense sectors, this technology provides critical advantages in secure communication, surveillance, and reconnaissance missions, where real-time, high-rate data transmission is essential. It also minimizes risks of detection and jamming in contested environments. In the commercial sector, airborne laser terminals enable fast, reliable communication for industries such as aviation, logistics, and telecommunications, improving operational efficiency and connectivity, particularly in remote or underserved areas.

There are several types of airborne laser terminal solutions tailored to different applications:

• Air-to-Air: These terminals facilitate high-speed, secure communication links between aircraft, ideal for military and defense operations requiring rapid data exchange in the airspace.

• Air-to-Ground: Airborne laser terminals for air-to-ground communication enable fast, high-rate data transfer from aircraft to users on the ground, providing a solution for intelligence, surveillance, and reconnaissance and other data-intensive applications.

• Air-to-Space: These terminals establish stable, high-speed optical communication links between aircraft and space-based systems, supporting satellite communication and enhancing connectivity for space-to-air networks.

The adoption of airborne laser terminals is primarily driven by:

• Rising Demand for High-Bandwidth, Secure Data Links in Defense Operations

• Growth of Constellations Driving Integration/Installation of Air-to-Space (A2S) Interfaces on Aircraft

• Supportive Government and Defense Modernization Programs

Challenges hindering the broader implementation of airborne laser terminal technology are:

• Atmospheric Interference and Weather Sensitivity

• Complex Certification and Regulatory Challenges

• High Development and Integration Costs

The global airborne laser terminal market was valued at $8.2 million in 2024 and is expected to grow at a CAGR of 17.30%, reaching $44.7 million by 2035. The growth is primarily driven by factors such as the increasing demand for high-bandwidth and secure data links in defense operations.

New entrants in the airborne laser terminal market should focus on:

• Developing Advanced Optical Components: Creating high-performance optical assemblies and subsystems that ensure robust pointing, acquisition, tracking, and turbulence tolerance will address the critical requirements for stable airborne laser communications.

• Standardization and Interoperability: Aligning products with established government standards, such as the Space Development Agency's Optical Communications Terminal specification, will enable smoother integration and reduce market entry barriers.

• Customization for UAVs and Defense Applications: Focusing on UAVs and defense applications, where high-rate data transfer is essential, while ensuring laser terminals are adaptable for future mission needs, will open niche opportunities.

• Strategic Partnerships and Government Contracts: Collaborating with defense contractors, government agencies, and aerospace organizations will secure contracts and foster long-term growth in this specialized, high-demand market.

This report is designed for stakeholders, including aerospace and defense companies, government agencies, technology providers, investors, and market analysts. It is particularly valuable for organizations seeking to explore growth opportunities in the airborne laser terminal market, understand the adoption of advanced optical communication systems, and identify strategic partnerships. Defense contractors and technology developers can benefit from insights into market trends, key challenges, and technological advancements, enabling them to make informed decisions on product development, investment strategies, and market positioning within this rapidly evolving sector.